Yaashvi Jewellers IPO Review (BSE SME)

Yaashvi Jewellers Ltd. (YJL) is engaged in manufacturing and trading of a wide range of jewellery with major product portfolio being gold jewellery in 9K, 14K, 18K, 20K, and 22K, focusing on affordability and quality. It is mainly engaged in machine made gold chains, which form the core of its product portfolio and are used in various jewellery designs. Alongside manufacturing, the company trades in studded gold and fashion silver jewellery, diamond jewellery, gold bullion, and also offer customized jewellery for clients.

The company is primarily engaged in the business of manufacturing of wide range of gold jewelleries which includes 9K, 14K, 18K, 20K, and 22K plain gold jewellery. It manufactures the finished gold jewelleries from the raw gold i.e., bullions and required consumables and further supply these products to dealers, showrooms, and small jewellery shops in the wholesale quantities as well as in retail. Its core specialization is in the manufacturing of machine-made gold chains which forms the major part of its product portfolio. Machine made gold chains are used in multiple formats, from being used as chain to be worn directly as final product or be used as part of larger jewellery such as mangalsutra, bracelets, anklets, earrings etc where it forms the base of the jewellery piece or used to provide the design element.

Machine-made gold chains are lightweight and can be crafted in a wide variety of designs and thicknesses, making them suitable for diverse customer needs. Additionally, depending on requirements, the company undertakes certain processes on job work basis and also outsources as needed. In addition to its core manufacturing operations, it is also engaged in the trading of a wide variety of jewellery products, catering to both wholesale and retail markets. its trading portfolio includes studded gold jewellery in 18K, 20K, and 22K, featuring designs that range from traditional to contemporary. The company also trades in diamond jewellery, offering both classic and modern designs to meet the growing demand for premium, high-value pieces.

In addition, it offers a range of fashion silver jewellery, available in gold-plated variants, catering to the rising demand for stylish and affordable accessories. YJL also trades in gold bullion, providing raw gold for investment or manufacturing needs. Additionally, it provides customized jewellery solutions in close collaboration with clients, ensuring each piece is tailored to their specific preferences and design requirements. If the requested design is not available in its existing collection, the company facilitates production through trusted job-workers to deliver the desired product with precision and quality. For the last two fiscals, its topline marked contribution from manufacturing activities for 72%, and trading activities around 28%. As of March 31, 2026, it had 65 employees on its payroll.

Issue Details / Capital History

The company is coming out with its maiden IPO of 5286400 equity shares of Rs. 10 each at a fixed price of Rs. 83 per share to mobilize Rs. 43.88 cr. The minimum application to be made is for 3200 shares and in multiples of 1600 shares thereon, thereafter. The issue opens for subscription on May 25, 2026 and will close on May 27, 2026. The shares will be listed on BSE SME. The IPO constitute 30% of the post-IPO paid-up capital of the company. The company is spending Rs. 4.84 cr. for this IPO process, and from the net proceeds of the equity issue, it will utilize Rs. 21.50 cr. for working capital, Rs. 11.00 cr. for repayment/prepayment of certain borrowings, and Rs. 6.54 cr. for general corporate purposes.

The IPO is solely lead managed by Smart Horizon Capital Advisors Pvt. Ltd., (erstwhile known as Shreni Capital Advisors Pvt. Ltd.), and Bigshare Services Pvt. Ltd. is the registrar to the issue. Cameo Corporate Services Ltd. is the RTA to the company. SHRENI Group’s Shreni Shares Ltd., is the market maker.

Having issued initial equity capital at par value, it has issued fresh shares in the price range of Rs. 18.50 – Rs. 123.00 per share between April 2024, and April 2025. The company also bonus shares in the ratio of 3 for 4 in January 2025. The average cost of acquisition of shares by the promoters is Rs. 1.70, and Rs. 7.38 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 12.34 cr. will stand enhanced to Rs. 17.62 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 146.26 cr.

IPO Lead Managers & Registrar

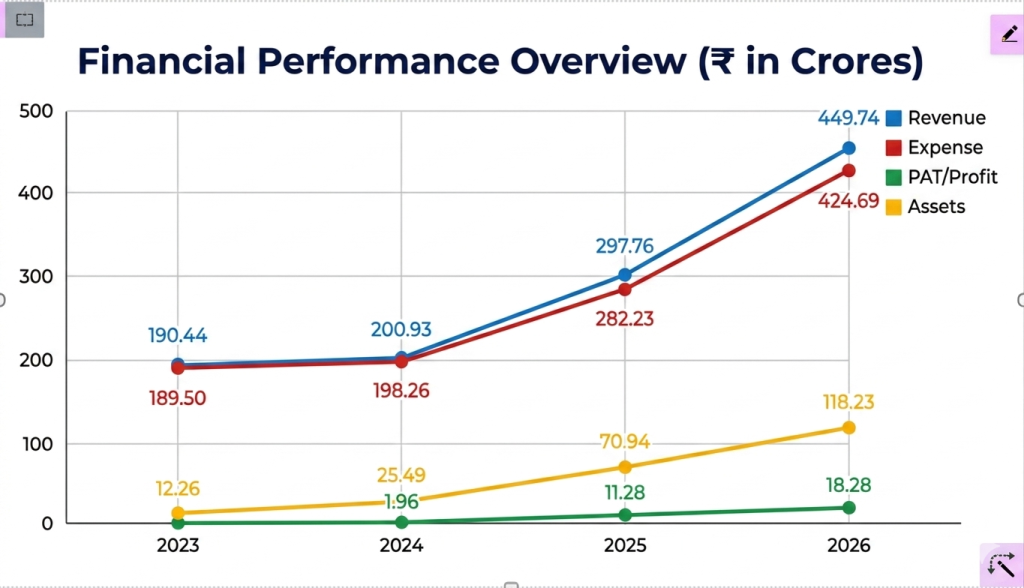

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 200.93 cr. / Rs. 1.96 cr. (FY24), Rs. 297.76 cr. / Rs. 11.28 cr. (FY25), Rs. 449.74 cr. / Rs. 18.28 cr. (FY26). Though it marked growth in its top and bottom lines, margins reported from FY25 onwards raise eyebrows as it is operating in a highly competitive and fragmented segment. Under the ongoing circumstances, maintaining of such margins appears to be a far-fetched dream.

For the last three fiscals, the company has reported an average EPS of Rs. 11.21 and an average RoNW of 40.33%. The issue is priced at a P/BV of 2.35 based on its NAV of Rs. 35.25 per share as of March 31, 2026, but its post-IPO NAV data is missing from the offer document.

If we attribute FY26 super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 8.02, and based on FY25 earnings, the P/E stands at 12.97. The issue appears fully priced based on its recent earnings, the margins appear inflated one to fetch fancy valuations for the IPO. In the given context, it will be hard to maintain the hefty margins and that may impact its immediate future trends.

The company has posted PAT Margins of 0.98% (FY24), 3.80% (FY25), 4.08% (FY26), and ROCE margins of 18.30%, 26.55%, 26.73%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has shown Ashapuri Gold, Moksh Gold, AJC Jewel, as its listed peers. They are trading at a P/E of 7.72, 10.8, and 20.2 (as of May XX, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

Merchant Banker's Track Record

This is the 25th mandate from Smart Horizon Capital in the last three fiscals (including the ongoing one). Out of the last 10 listings, 3 opened at discount, 1 at par, and the rest listed with premiums ranging from 0.28% to 10% to offer price on listing date. The merchant banker has an average track record.

Conclusion

YJL is engaged in the manufacturing and trading in wide range of jewellery with major product portfolio. It provides jewellery in 9K, 14K, 18K, 20K, and 22K focusing affordability and quality. The company marked growth in its top and bottom lines for the reported periods. Surge in its bottom lines appears to be inflated one to fetch fancy valuation for the IPO. Based on its recent financial data, the issue appears. There is no harm in skipping this fully priced offer at this juncture amidst ongoing scenario.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.