M R Maniveni Ltd. (MRML) has an established track record of over 15 years in the food industry, specializing in the milling, processing, and supply of pulses, primarily urad dal and toor dal. It commenced operations in 2010 with a focus on milling urad dal and trading a diversified range of products including urad dal, toor dal, moong dal, kabuli channa, green gram dal, coriander seeds, rice, and chilies. This product diversification enabled it to serve a wider customer base, strengthen its presence in the pulses segment, and build industry experience across multiple categories.

In the initial years, milling was carried out through manual processes for urad dal. In 2022, recognizing the increasing demand for urad dal, the company transitioned to automation by installing advanced automatic machinery requiring minimal human intervention. This enhanced production efficiency, consistency, and quality assurance. In 2023, MRML further expanded its operations by introducing the milling of toor dal through a semi-manual process, blending traditional methods with selective mechanization to retain flexibility in operations.

The company currently operates two dedicated milling facilities – 1) automated, and 2) Semi-automated. This dual facility model provides it with the ability to balance scalability through automation with operational flexibility, thereby catering to both bulk institutional buyers and specialized demand segments. Its business model is predominantly business-to-business (B2B). It supplies its processed pulses to large-format retailers, wholesalers, and e-commerce platforms, who subsequently serve the end consumers. This model enables the company to maintain long term institutional relationships, achieve bulk supply efficiencies, and benefit from consistent demand visibility. Its competitive advantage lies in delivering clean, well-milled, and contamination-free products that align with stringent customer expectations on quality and hygiene. As of April 30, 2026, it had 16 employees on its payroll.

The company is coming out with its maiden book building route IPO of 5200000 equity shares of Rs. 10 each to mobilize Rs. 27.04 cr. The company has announced price band of Rs. 51 – Rs. 52 per share of Rs. 10each. The minimum application to be made is for 4000 shares and in multiples of 2000 shares thereon, thereafter. The issue opens for subscription on May 22, 2026 and will close on May 26, 2026. The shares will be listed on BSE SME. The IPO constitute 26.57% of the post-IPO paid-up capital of the company. From the net proceeds of the equity issue, it will utilize Rs. 13.61 cr. for capex on new plant and machineries, Rs. 12.69 cr. for capex on new factory construction, and the rest for general corporate purposes.

The IPO is solely lead managed by CapitalSquare Advisors Pvt. Ltd., and Bigshare Services Pvt. Ltd. is the registrar to the issue. CapitalSquare Group’s CapitalSquare Financial Services Pvt. Ltd., is the market maker and a syndicate member.

The company has issued initial equity capital at par value, it has issued fresh shares at a price of Rs. 70 per share in December 2024. The company also bonus shares in the ratio of 2 for 1 in October 2024, and 1 for 1 in December 2024. The average cost of acquisition of shares by the promoters is Rs. 1.90, Rs. 2.55, and Rs. 3.79 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 14.37 cr. will stand enhanced to Rs. 19.57 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 101.78 cr.

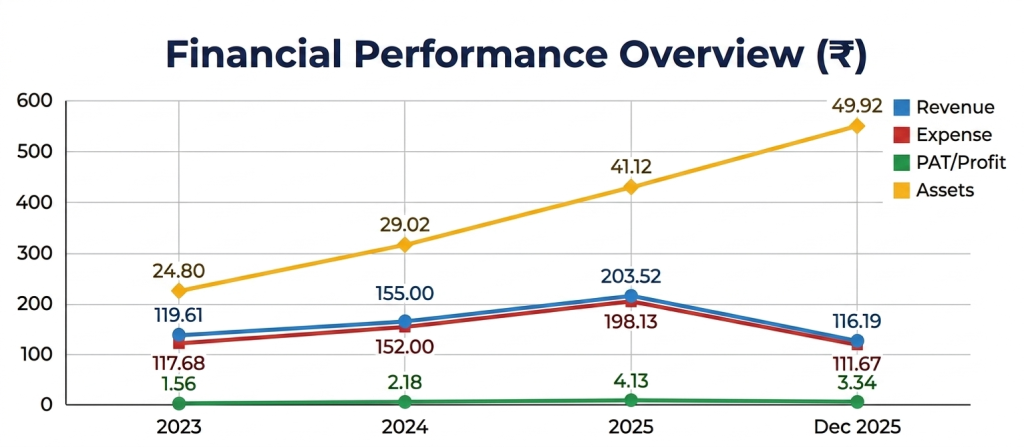

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 119.61 cr. / Rs. 1.56 cr. (FY23), Rs. 155.00 cr. / Rs. 2.18 cr. (FY24), Rs. 203.52 cr. / Rs. 4.13 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 3.34 cr. on a total income of Rs. 116.19 cr. The company marked quantum jump in its top and bottom lines for FY23 and FY25. Sustainability of such margins going forward remains concern, as it is operating in a highly competitive and fragmented segment.

For the last three fiscals, the company has reported an average EPS of Rs. 2.19 and an average RoNW of 23.49%. The issue is priced at a P/BV of 3.49 based on its NAV of Rs. 14.89 per share as of December 31, 2025, but its post-IPO NAV data is missing from the offer documents.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 18.98, and based on FY25 earnings, the P/E stands at 24.64. The issue appears aggressively priced based on its recent earnings and also in comparison to its listed peers for posting higher margins.

The company has posted ROCE Margins of 13.24% (FY23), 14.50% (FY24), 17.14% (FY25), 12.58% (9M-FY26), and PAT margins of 1.30%, 1.41%, 2.03%, 2.87%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown Sameera Agro, and Jeyyam Global, as its listed peers. They are trading at a P/E of 2.86, and 6.47 (as of May 19, 2026). However, they are not truly comparable on an apple-to-apple basis.

This is the 4th mandate from CapitalSquare Advisors in the last two fiscals (including the ongoing one). Out of the last 3 listings, all listed at a discount to offer price on listing date. The Lead Manager has a poor track record so far.

MRML is engaged in the business of milling, processing and supply of pulses, and other agri commodities. It had adopted automatic and semi-automatic milling units to scale up its operations. It posted growth in its top and bottom lines for the reported periods. Based on its recent financial data/earnings, the issue appears aggressively priced. It is operating in a highly competitive and fragmented segment, and that may not permit such higher margins. Merchant Banker has a poor track record. There is no harm in skipping this pricey offer.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.