CMR Green Ltd. Technologies (CGTL) is the leading non-ferrous metal recycler in terms of installed capacity as of March 31, 2025 and it has the highest market share in the Indian secondary aluminium market in terms of revenue from operations for the Fiscal 2025 amongst the peer companies (Source: ICRA Report). CGTL has a capacity advantage over domestic players, with an installed capacity of around 4 times of the nearest competitor in the domestic recycled aluminium space, as of March 31, 2025 (Source: ICRA Report). The company ranks among the largest players in the global aluminium recycling industry in terms of installed capacity as of March 31, 2025 (Source: ICRA Report). It manufactures recycled aluminium alloys (in ingot and liquid form), zinc alloy ingots, dross and segregated furnace ready scrap of stainless steel, copper, brass, zinc, lead and magnesium, amongst others.

CGTL recycles used beverage cans scrap for fulfilling new metal requirements of primary producers. Due to the large economic, environmental and social advantages of recycling and the disadvantages of mining, primary producers across the world are shifting to develop new sources of recycled metal (Source: ICRA Report). The Company also produces aluminium billets that cater to both automotive and non-automotive sectors. These billets, made from recycled aluminium, are raw materials used in extrusion processes to create profiles for various applications. Its billets are manufactured to meet industry standards, ensuring stable mechanical properties, formability, and corrosion resistance. In Fiscal 2025, the total recycled aluminium market reached a volume of 2.16 million MT in India. Of this, 1.01 million MT (46.7%) was from the cast alloy segment, 0.59 million MT (27.5%) was in rolled segment and 0.34 million MT (15.6%) was in extrusion segment.

While it is currently present in the cast alloy segment of the automotive industry (where it has approximately 42-45% market share in terms of volume sold for Fiscal 2025 as per ICRA Report), its entry into the extrusion has expanded serviceable market by a further 0.34 million MT and rolled alloy segments have expanded its serviceable market by further 0.59 million MT, providing new growth opportunities (Source: ICRA Report). With its new plants in Tirupati and Odisha, the company is now positioned to address a wider spectrum of aluminium products within the recycling value chain. Aluminium is endlessly recyclable without any loss in quality, making it an ideal material for sustainable industrial use (Source: ICRA Report). India’s primary aluminium industry emits 14 tonnes of CO₂ per ton of aluminium, one of the highest rates globally, whereas recycled aluminium emits only 0.3 ton. (Source: ICRA Report)

Additionally, secondary aluminium production has approximately 90% lower capital expenditure (capex) intensity compared to primary production, making it the most cost-effective pathway to decarbonizing the industry. (Source: ICRA Report). Aluminium recycling has a lion share in CGTL’s total revenue (around 82% for 9M-FY26) and the rest is from other metals/materials. Top 10 customers are contributing little over half in its top lines. As of December 31, 2025, it had 784 employees on its payroll and additional 3956 contract workers in various departments.

The company is coming out with its maiden book building route secondary IPO of 32858323 equity shares of Rs. 2 each to mobilize Rs. 630.88 cr. at the upper cap. The IPO is entirely as an Ofer for Sale (OFS); hence no funds are going to the company. The company has announced a price band of Rs. 182 – Rs. 192 per equity shares of Rs. 2 each. The issue opens for subscription on June 03, 2026, and will close on June 05, 2026. The minimum application to be made is for 78 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 15% of the post-IPO paid-up equity capital. The OFS is being made to unlock its value, provide exit to its stakeholders and listing benefits.

The company has reserved 130182 equity shares (worth Rs. 2.50 cr. at the upper cap) for its eligible employees and offering them a discount of Rs. 18 per share. From the rest, it has allocated not more than 50% for QIBs, not less than 15%for HNIs, and not less than 35% for Retail investors.

The joint Book Running Lead Managers (BRLMs) to this issue are Equirus Capital Ltd., ICICI Securities Ltd., and Motilal Oswal Investment Advisors Ltd., while KFin Technologies Ltd., is the registrar to the issue. Equirus Securities Pvt. Ltd., and Motilal Oswal Financial Services Ltd., are the syndicate members.

The company has issued/converted initial equity shares at par value. It has also issued bonus shares in the ratio of 11 for 1 in September 2021. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. NIL, Rs. 0.01, Rs. 0.02, Rs. 0.05, and Rs. 0.08 per share.

Post-IPO, its current paid-up equity capital of Rs. 43.81 cr. will remain same as this is a pure secondary issue. Based on the upper band of price, the company is looking for a market cap of Rs. 4205.87 cr.

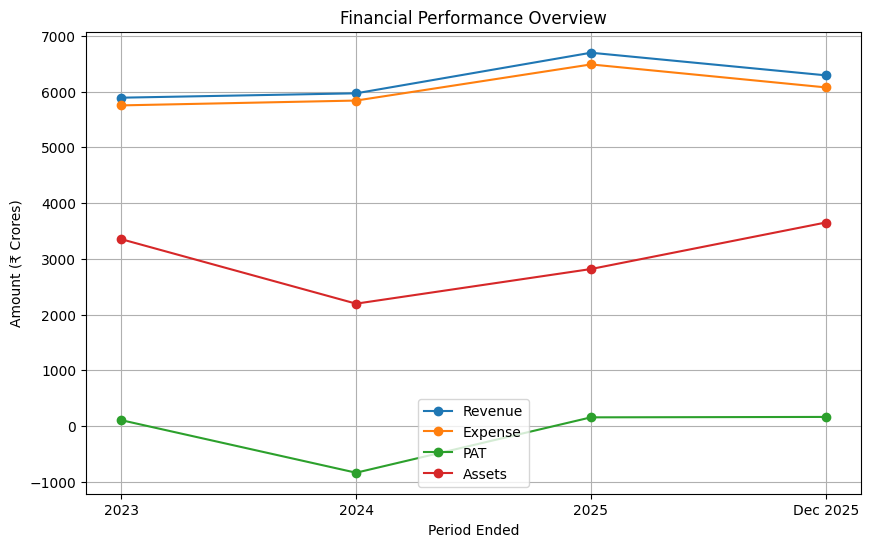

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted a total income/net profit/ - (loss), of Rs. 5889.90 cr. / Rs. 104.51 cr. (FY23), Rs. 5968.44 cr. / Rs. – (838.56) cr. (FY24), and Rs. 6696.66 cr. / Rs. 155.04 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 162.39 cr. on a total income of Rs. 6291.00 cr. Drastic fall in its bottom line to a negative level for FY24 is attributed to exceptional items provision which was no longer needed. The company has cleaned its balance sheet and is poised for bright prospects ahead with ongoing expansion spree.

For the last three fiscals, the company has posted an average EPS of Rs. – (8.70) and an average RoNW of – (71.73) %. The issue is priced at a P/BV of 7.08 based on its NAV of Rs. 27.12 as of December 31, 2025, as well as on post IPO basis.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 19.43. Based on FY25 earnings, the P/E stands at 27.12. The issue appears fully priced based on its recent financial data.

For the reported periods, while the company has posted PAT margins of 1.77% (FY23), - (14.05) % (FY24), 2.32% (FY25), 2.59% (9M-FY26), but its RoCE margins data is missing from the offer document.

All amounts in Indian Rupees crores

The company not paid any dividends for the reported periods of the offer document. It has already adopted a dividend policy in August 2025, based on its financial performance and future prospects.

As per the offer document, the company has shown Pondy Oxides, Gravita India, Baheti Recycling, Jain Resource, as its listed peers. They are currently trading at a P/E of 28.1, 31.4, 22.8, and 36.6 (as of May 29, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

The three BRLMs associated with this issue have handled 77 issues in the last 3 fiscals (including the ongoing one), out of which 25 issues closed below the offer price on listing date.

CGTL is one of the leading non-ferrous metal recyclers enjoying highest market share in secondary aluminium market. It has the largest capacities among the industry players and enjoys most preferred partner status. The company marked losses for FY24 following adjustments of exceptional item. It posted growth in its top lines for the reported periods. The issue appears fully priced based on its recent financial data. Investors can park funds for medium to long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.