Aureate Tradde Ltd. (ATL) is engaged in trading, distribution, and supply of industrial and technological materials across three key business verticals: (i) Polymers and Petrochemicals; (ii) Lithium-ion and Sodium-ion Cells, and; (iii) Electric Vehicle Chargers. The company’s business operates on "Inventory-based model”, which means it purchases and maintains stock in advance, enabling it to efficiently serve a wide array of customers, including small, medium, and large enterprises. By offering a diverse range of products, ATL caters to wide range of customer base and increase its ability to meet the varied needs of the industries it serves.

Its operational model relies primarily on rented warehouse facilities, its inventory management strategy is built on strong partnership and stringent reconciliation protocols. The physical control and management of all polymer and cell inventory are the direct responsibility of the Warehouse Company operating the rented facility. This includes material receipt, storage, handling, picking and dispatch. ATL relies on the Warehouse Company's systems to ensure inventory updates are regularly provided and maintained. Its internal stock records (the "stock in its books") are consistently updated and tallied against the physical stock counts reported by the warehouse company. This ongoing reconciliation process is mandatory to ensure that the physical inventory matches the quantities reflected in its ledgers and financial statements, providing it with accurate, validated stock data without maintaining proprietary storage infrastructure. The company has obtained requisite insurance for the products kept in such warehouses.

At present, the company is primarily involved in domestic B2B market for trading and distribution of polymer, petrochemicals, Lithium-ion cells and Sodium-ion cells. Additionally, it also operates in B2B and B2C segment for trading and distribution of Electric Vehicle Chargers. Through its strong relationships with suppliers and customers, the company has built a reliable and efficient customs. Its business is based on prudent inventory management, disciplined financial control, strict Quality Assurance Standards and a deep understanding of its customers' needs.

At present, ATL is the sole and exclusive distributor of Sodium-ion Cells in PAN India, for a well-established international Manufacturing Company i.e., Jianghu Highstar Battery Manufacturing Co., Ltd. specialized in the R & D, production, and sales of secondary chemical power and related compounds. As of April 30, 2026, it had 13 employees on its payroll.

The company is coming out with its maiden IPO of 3898000 equity shares of Rs. 10 each at a fixed price of Rs. 70 per share to mobilize Rs. 27.29 cr. The minimum application to be made is for 4000 shares and in multiples of 2000 shares thereon, thereafter. The issue opens for subscription on May 29, 2026 and will close on June 02, 2026. The shares will be listed on BSE SME. The IPO constitute 30.02% of the post-IPO paid-up capital of the company. The company is spending Rs. 3.27 cr. for this IPO process, and from the net proceeds of the issue, it will utilize Rs. 9.93 cr. for repayment/prepayment of certain borrowings, Rs. 10.00 cr. for working capital, and Rs. 4.09 cr. for general corporate purposes.

The IPO is solely lead managed by Corporate Makers Capital Ltd., and MUFG Intime India Pvt. Ltd. is the registrar to the issue. Giriraj Stock Broking Pvt. Ltd., is the market maker. The IPO is underwritten to the tune of 15.03% by Corporate Makers Capital, and 84.97% by Giriraj Stock Broking.

Having issued initial equity capital at par value, it has issued further equity shares in the price range of Rs. 252.00 – Rs. 1474.00 per share between March 2021 - March 2024. The company also bonus shares in the ratio of 473 for 5 in September 2025. The average cost of acquisition of shares by the promoters is Rs. 5.95, and Rs. 10.38 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 9.09 cr. will stand enhanced to Rs. 12.99 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 90.90 cr.

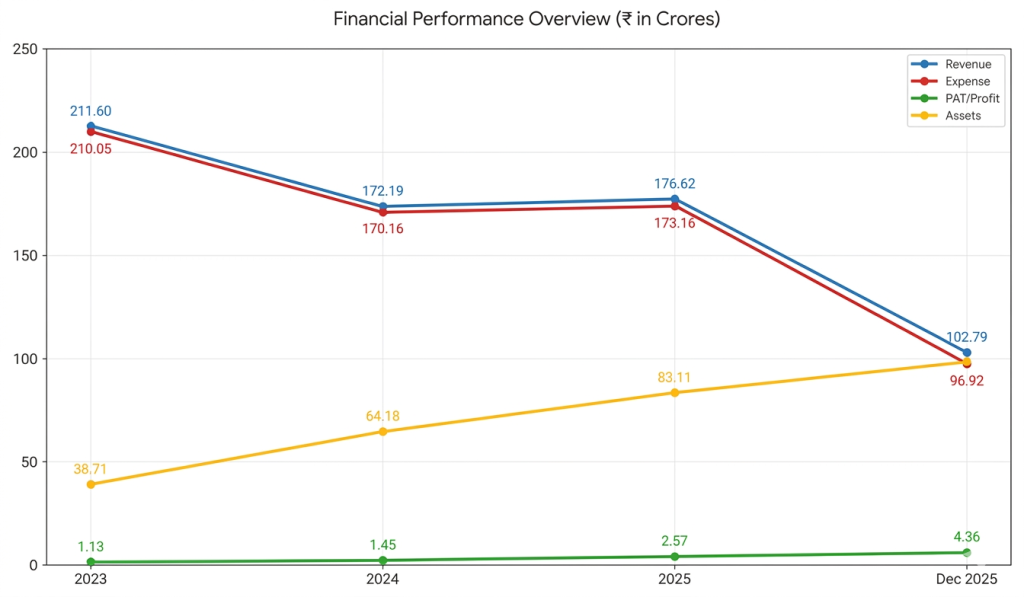

On the financial performance front, for the last three fiscals, the company has posted total revenue/ net profit, of Rs. 211.60 cr. / Rs. 1.13 cr. (FY23), Rs. 172.19 cr. / Rs. 1.45 cr. (FY24), Rs. 176.62 cr. / Rs. 2.57 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 4.36 cr. on a total revenue of Rs. 102.79 cr. which a big surprise posted by the company that appears to be the inflated earnings. It marked degrowth in its top lines for FY24, and a minor surge for FY25, but its bottom line kept improving.

For the last three fiscals, the company has reported an average EPS of Rs. 2.16 and an average RoNW of 21.19%. The issue is priced at a P/BV of 3.69 based on its NAV of Rs. 18.98 per share as of December 31, 2025, and at a P/BV of 2.04 based on its post IPO NAV of Rs. 34.29 per share.

If we attribute FY26 super annualized earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 15.66, and based on FY25 earnings, the P/E stands at 35.35. The issue appears aggressively priced based on its recent overall earnings.

The company has posted PAT Margins of 0.54% (FY23), 0.85% (FY24), 1.48% (FY25), 4.28% (9M-FY26), and ROCE margins of – (0.91) %, 17.87%, 20.56%, 25.07%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown Bhavik Enterprises, as its listed peer. It is currently trading at a P/E of 96.1 (as of May 26, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears to be an eyewash.

This is the 8th mandate from Corporate Makers in the last three fiscals (including the ongoing one). Out of the last 7 listings, 5 listed at discount, 2 at par. Thus, the lead manager has a poor track record so far.

ATL is engaged in trading, distributing, supply of industrial and technological materials. It deals with three business verticals, i.e., polymers/petrochemicals, lithium-ion and sodium-ion cells, and electric vehicle chargers. The company posted inconsistency in its top lines for the reported periods. It posted surge in its bottom line year-on-year, but the bumper earnings for 9M-FY26 is a big surprise. Based on its recent financial data, the issue appears aggressively priced. Merchant banker has a poor track record. There is no harm in skipping this pricey and dicey IPO.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.