Waterways Leisure Tourism Ltd. (WLTL) is one of the domestic ocean cruise operators in India (Source: CRISIL Report), offering luxurious and inherent Indian experiences. The company believes this enables it to set industry benchmarks, foster brand loyalty, and establish pricing standards, thereby strengthening its market presence and creating a strong competitive position. The company currently operate a cruise vessel, the ‘MV Empress’, and since its launch, 730,819 guests have sailed on its cruise vessel, which has covered more than 321,292.53 nautical miles along the Indian coastline and surrounding islands as of March 31, 2026.

In Fiscal 2025, WLTL accounted for approximately 79% of the market share in value terms. (Source: CRISIL Report) Its cruise vessel primarily sails to domestic destinations such as Mumbai (Maharashtra), Goa, Kochi (Kerala), Chennai (Tamil Nadu), Lakshadweep, Visakhapatnam (Andhra Pradesh), and Puducherry. The company has in the past and continue to offer international itineraries to Hambantota, Trincomalee, and Jaffna (Sri Lanka), Phuket (Thailand), Singapore, Kuala Lumpur and Langkawi (Malaysia). Its itineraries are designed to showcase India’s coastal regions and cultural heritage, providing guests with an enriching travel experience and establishing itself as the go-to choice for luxury and cultural cruising. Its cruise vessel ‘MV Empress’ offers a variety of cabin options, including one chairman’s suite, five suites, 63 mini suites, 416 ocean-view staterooms, and 311 interior staterooms, totalling 796 cabins, with prices ranging from Rs. 34164 (interior rooms) per night to Rs. 151,111 (Chairman suite) per night, subject to dynamic pricing and load factor considerations.

WLTL’s cruise experience is designed to cater to the preferences of Indian guests and international travellers visiting India, offering an immersive journey into India’s rich culture, cuisine, and warm hospitality. Every aspect of the voyage is curated to provide an authentic Indian experience, ensuring that guests feel the essence of India while sailing. It offers a diverse culinary experience, providing a variety of food options such as pan-Asian, international, and Indian cuisine, including Jain food options. The company also organize live performances and themed shows inspired by Indian Cinema such as ‘Indian Cinemagic’, ‘Balle Balle’, ‘Burlesque – Bollywood Way’, ‘Razzmatazz’, and ‘Romance in Bollywood’. It offers a wide range of amenities for all age groups, including a children’s academy, gaming arcade, spa and salon, retail outlets, casino, fitness center, a rock-climbing wall, and swimming pools. The company also offers specialized arrangements for Meetings, Incentives, Conferences, and Exhibitions (“MICE”) events and weddings, with comprehensive services that include venue arrangements, catering, entertainment, and accommodation.

It has strategically outsourced critical cruise operations to enhance efficiency and scalability. The company leverages third-party expertise in areas such as food and beverages, housekeeping, crewing, and entertainment. This enables it to tap into their knowledge and resources, ensuring quality service delivery. This flexibility also enables it to scale its operations based on seasonal demand, manage resources effectively and maintain service standards. Outsourcing allows it to concentrate on its core activities, ensuring an enhanced customer experience and expanding our cruise offerings.

WLTL’s guests have options to book their cabins either directly with it through its website, mobile application and over the phone, or through third-party travel agents. Historically, a majority of its cabins have been booked directly, reflecting its guests’ trust and preference for its straightforward and efficient booking process. For the Fiscal 2026, 2025 and 2024, the company directly sold 62.25%, 62.98% and 59.96% of the total cabins, respectively. Direct bookings reduce commissions paid to travel agents and improve its margins. It also provides an additional opportunity to directly engage with its guests, enabling it to strengthen brand awareness and deliver a more personalized and memorable experience. As of March 31, 2026, its direct booking is supported by its call centers, which employs 148 cruise holiday experts. Their contribution enhances the efficiency and effectiveness of its direct sales, ensuring seamless customer interactions and booking experiences. As of March 31, 2026, it had 245 employees on its payroll.

The company is coming out with its maiden book building route primary IPO of 7240099 equity shares of Rs. 10 each to mobilize Rs. 585.00 cr. at the upper cap. The company has announced a price band of Rs. 769 – Rs. 808 per equity shares of Rs. 10 each. The issue opens for subscription on June 23, 2026, and will close on June 25, 2026. The minimum application to be made is for 18 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 10% of the post-IPO paid-up equity capital. From the net proceeds of the IPO, the company will utilize Rs. 480.01 cr. for payment towards deposit/advanced lease rental, monthly lease payents to its step-down subsidiary – Baycruise Shipping and Leasing (IFSC) Pvt. Ltd., and the rest for general corporate purposes.

The company has allocated atlease75% for QIBs, not more than 15% for HNIs and not more than 10% for Retail investors.

The sole Book Running Lead Manager (BRLM) to this issue is Centrum Broking Ltd., and MUFG Intime India Pvt. Ltd., is the registrar to the issue. Centrum Broking is also a syndicate member.

The company has issued entire equity shares at par value. The average cost of acquisition of shares by the promoters is Rs. 10.00 per share.

Post-IPO, its current paid-up equity capital of Rs. 65.15 cr. will stand enhanced to Rs. 72.39 cr. Based on the upper cap of the price band, the company is looking for a market cap of Rs. 5849.48 cr.

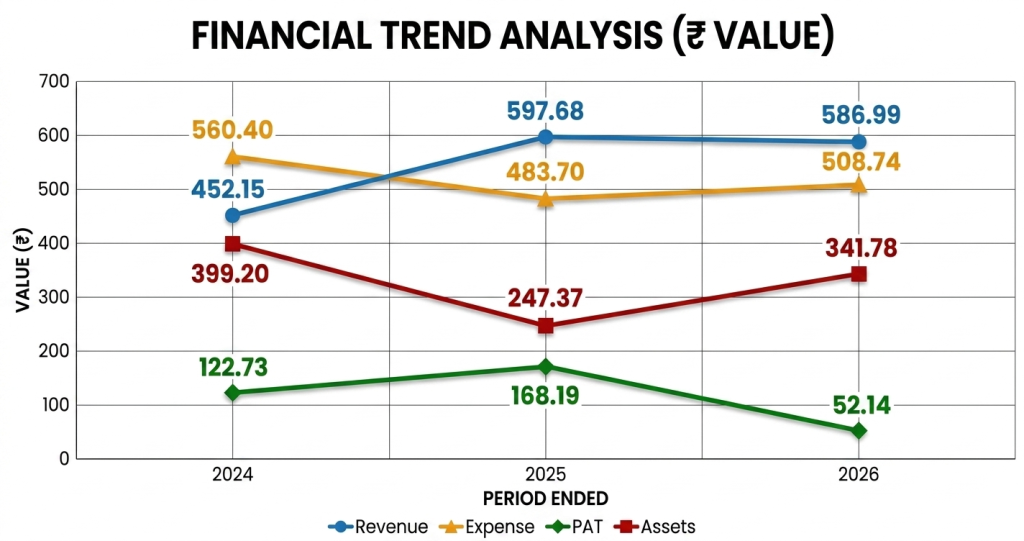

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted a total income/net profit/ - (loss), of Rs. 452.15 cr. / Rs. – (122.73) cr. (FY24), Rs. 597.68 cr. / Rs. 168.19 cr. (FY25), and Rs. 586.99 cr. / Rs. 52.14 cr. (FY26). It marked de-growth in its top and bottom lines for FY26, that raise concern. Its contingent liabilities of Rs. 25.20 cr. for Income Tax matter, as of March 31, 2026, raise alarm. Around 90% revenue comes from Cruise Ticket Sales, and rest from onboard revenue, commission, etc.

For the last three fiscals, the company has posted an average EPS of Rs. 9.52 and an average RoNW of 214.06 %. The issue is priced at a P/BV of 65.64 based on its NAV of Rs. 12.31 as of March 31, 2026, and at a P/BV of 72.92 based on its post-IPO NAV of Rs. 11.08 per share at the upper cap. Its higher debt-equity ratio of 1.27 as of March 31, 2026 raise alarm.

If we attribute FY26 earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 112.22. Based on FY25 earnings, the P/E stands at 34.78. The issue appears aggressively priced based on its recent financial data.

For the reported periods, the company has posted PAT margins of – (0.27) times (FY24), 0.28 % times (FY25), 0.09% times (FY26), and RoCE margins of 0.62 times, 5.03 times, 1.14 times, respectively for the referred periods.

All amounts in Indian Rupees crores

As per the offer document, the company has shown surprising list of listed peers i.e, Chalet Hotels, Lemon Tree, Juniper Hotels, Samhi Hotels, Taj GVK, Wonderla Holidays, Imagicca World, (on domestic level) and Royal Caribbean, Carnival Corp., Norwegian Cruise Line (on outside India). They are currently trading at a P/E of 26.8, 36.2, 25.9, 9.50, 13.7, 35.8, and 3985.0 (as of June 18, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

As per the offer document, the company has shown Bluestone Jewellery, RBZ Jewellers, Radhika Jeweltech, as its listed peers. They are currently trading at a P/E of 517.0, 9.69, and 9.03 (as of June 18, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

The sole BRLM associated with this issue has handled 3 issues in the last 3 fiscals (including the ongoing one), out of which 2 issues closed below the offer price on listing date. The merchant banker has poor track record.

WLTL is one of the domestic ocean cruise operators in India, offering luxurious and inherent Indian experiences. It appears its top line has come to a saturation level as for the last three fiscals, it posted almost static top line for the last two fiscals. Declined top and bottom lines for FY26 remains a major concern. Its debt-equity ratio of 1.27 as of March 31, 2026 raise alarm. Based on its recent financial data, the issue appears exorbitantly priced. There is no harm in skipping this pricey and dicey IPO.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.