Liotech Industries Ltd. (LIL) specializes in the production of hardware structures and accessories, including door kits, a wide range of hinges (including cut & butt, parliament, W, Z, and duck hinges), gate hooks, aldrop, locks, handles, tower bolts, and shelf bottoms. It offers a diverse selection of products, with over 150 distinct specifications, that cater to various industries such as housing, infrastructure, agriculture, automotive, electricity, cement, mining, solar energy, and general engineering. The company adheres to a business-to-business (B2B) operational framework. Aside from its production operations, the company also engage in the trading of supplementary products such as door stoppers, magnets, table brackets, bed lifters, and bell magnets.

LIL owns and operates a manufacturing unit located in Rajkot, Gujarat, spanning 12,632 square feet. This facility is strategically situated to offer locational advantages, enabling us to meet customers' just-in-time delivery schedules, achieve economies of scale, and provide logistical benefits to customers, thereby protecting them from local supply disruptions. The company provides end-to-end product solutions that include designing, manufacturing, quality testing, packaging, and logistics under the B2B model. It has installed a diverse array of plant and machinery at manufacturing facility to facilitate the fabrication and production of a diverse selection of products. As of December 31, 2025, it had 16 employees on its payroll. It hires contract workers as and when needed.

The company is coming out with its maiden combo IPO of 1122000 equity shares of Rs. 10 each at a fixed price of Rs. 321 per share to mobilize Rs. 36.02 cr. The IPO consists of 900000 fresh equity shares worth Rs. 28.89 cr., and an Offer for Sale (OFS) of 222000 equity shares worth Rs. 7.13 cr. The minimum application to be made is for 800 shares and in multiples of 400 shares thereon, thereafter. The issue opens for subscription on June 01, 2026 and will close on June 03, 2026. The shares will be listed on BSE SME. The IPO constitute 28.77% of the post-IPO paid-up capital of the company. The company is spending Rs. 4.61 cr. for this IPO process (Fresh equity issue portion only), and from the net proceeds of the issue, it will utilize Rs. 4.95 cr. for repayment/prepayment of certain borrowings, Rs. 7.00 cr. for working capital, Rs. 8.00 cr. for acquiring machinery, and Rs. 4.33 cr. for general corporate purposes.

The IPO is solely lead managed by Wealth Mine Networks Pvt. Ltd., and KFin Technologies Ltd. is the registrar to the issue. Aikyam Capital Pvt. Ltd., is the market maker. The IPO is underwritten to the tune of 15.00% by Wealth Mine Networks, and 85.00% by Aikyam Capital.

The company has issued entire initial equity capital at par value. The average cost of acquisition of shares by the promoters is Rs. 0.00, and Rs. 20.00 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 3.00 cr. will stand enhanced to Rs. 3.90 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 125.19 cr.

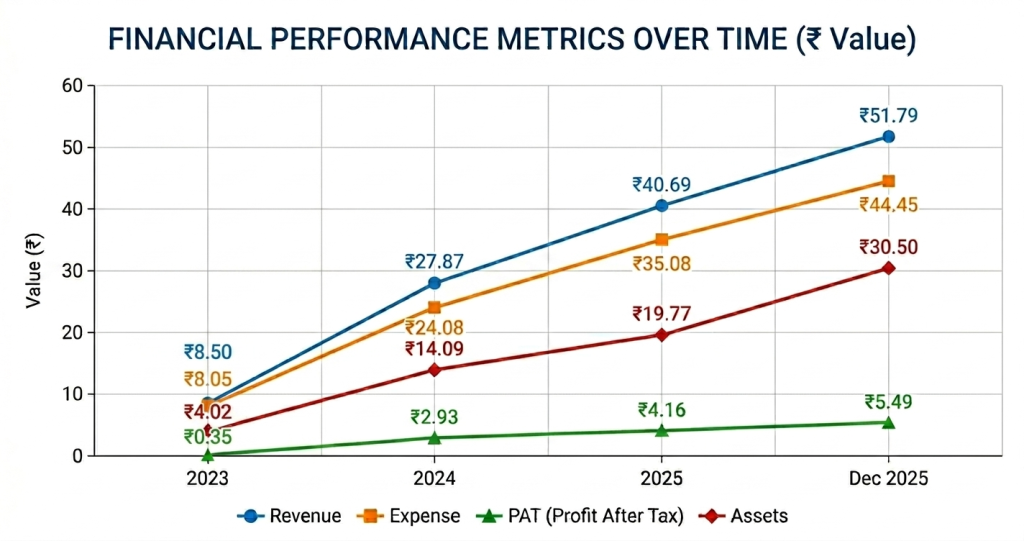

On the financial performance front, for the last three fiscals, the company has posted total revenue/ net profit, of Rs. 8.50 cr. / Rs. 0.35 cr. (FY23), Rs. 27.87 cr. / Rs. 2.93 cr. (FY24), Rs. 40.69 cr. / Rs. 4.16 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 5.49 cr. on a total revenue of Rs. 51.79 cr. which a big surprise posted by the company. It marked growth in its top lines from FY24 onwards but sudden boost in its profit margins raises eyebrows.

For the last three fiscals, the company has reported an average EPS of Rs. 10.87 and an average RoNW of 37.90%. The issue is priced at a P/BV of 6.04 based on its NAV of Rs. 53.12 per share as of December 31, 2025, and at a P/BV of 2.79 based on its post IPO NAV of Rs. 114.94 per share.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 17.11, and based on FY25 earnings, the P/E stands at 30.06. The issue appears aggressively priced based on its recent earnings.

The company has posted PAT Margins of 4.06% (FY23), 10.50% (FY24), 10.24% (FY25), 10.64% (9M-FY26), and ROCE margins of 14.75%, 47.53%, 50.43%, 44.45%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends since its incorporation. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has no listed peers to compare with.

This is the 4th mandate from Wealth Mine in the last two fiscals (including the ongoing one). Out of the last 2 listings, all listed at discount. Thus, the lead manager has a poor track record so far. The last IPO of SMR Jewel Ltd. yet to be listed.

LIL is engaged in the manufacturing and marketing of specialized hardware structures and accessories including related products basket. The company operates on a B2B model operations. The company posted growth in its top and bottom lines for the reported periods. The boost in its margins from FY24 onwards raise eyebrows and concern over its sustainability as it is operating in a highly competitive and fragmented segment. Based on its recent financial data, the issue appears aggressively priced. Tiny post-IPO equity capital indicates longer gestation for migration. There is no harm in skipping this pricey and dicey IPO.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.