Laser Power & Infra Ltd. (LPIL) is an integrated manufacturer of power cables, conductors and other specialised products and components to the power transmission and distribution industry in India. With an established operating history spanning over three decades, it has built a strong reputation for delivering high-quality products tailored to the evolving needs of clients and tailor-made for their projects. In furtherance of its forward integration strategy, in the year 2015, the company strategically expanded business by entering the engineering, procurement, and construction (“EPC”) segment in power distribution sector, focusing on rural electrification projects, power distribution infrastructure development, and installation of substations, among other turnkey solutions.

According to CRISIL, LPIL is one of the leading players in terms of manufacturing capacity of 85448 MT for power cables and conductors in Fiscal 2026, among the power cable and conductor players having manufacturing facilities of power cable and conductors in East India. It is a registered supplier to Indian Railways, accredited by the Research Design & Standard Organization (“RDSO”) and one of the largest approved vendors of PVC insulated armoured unscreened underground power cable, quad cables for signal and telecommunication (“S&T”) installations and PVC insulated armoured unscreened underground railway signalling cable, signalling control, quad and power cables based on capacities of these products, among the approved vendors in East India. (Source: CRISIL Report)

The company operates three Manufacturing Units each located at West Bengal, India, which have a combined installed capacity of 85448 MT, as of March 31, 2026. Two of its manufacturing units (“Manufacturing Unit I”) and (“Manufacturing Unit II”) are located at Dhulagarh, West Bengal. Its Manufacturing Unit I is dedicated for the manufacturing of high tension (“HT”) power cables, RDSO signalling control, quad cables and conductors, and Manufacturing Unit II focuses on manufacturing of aluminium wire rods and HT covered conductors. LPIL’s third manufacturing unit is located at Kharagpur, West Bengal and is dedicated for the manufacturing of low tension (“LT”) aerial bunched cables, LT power cables and aluminium conductor steel reinforced (“ACSR”) conductors (“Manufacturing Unit III”, collectively with Manufacturing Unit I and Manufacturing Unit II, referred as the “Manufacturing Units”). Its Manufacturing Units are strategically located near key ports in Kolkata and Haldia, providing logistical advantages for both domestic and international markets.

The strategic location of Manufacturing Units in eastern part of India serves as a major advantage in terms of close proximity to raw material sources including aluminium and copper, which further ensures easy and cost-effective procurement of raw material, improves overall operational efficiency and reduce lead times. Its Manufacturing Units adhere to stringent quality control measures and international standards, ensuring the delivery of high-quality products. The company strives to deliver customized and innovative products with speed and quality service. Its Manufacturing Units are certified for ISO 9001, ISO 14001 and ISO 45001 standards. Its Manufacturing Units are equipped with modern machinery and testing systems conforming to Bureau of Indian Standards (“BIS”) and other international benchmarks.

LPIL’s Manufacturing Units are critical to its integrated approach, which enables it to leverage in-house production capacities, supply chain efficiency, and technical expertise to deliver cost-effective, high-quality solutions tailored to client and project-specific requirements. It has built long-standing relationships with key public sector and private clients. The company serves a number of reputed government authorities including Indian Railways, various distribution companies (“DISCOMS”) including TP Central Odisha Distribution Limited, TP Western Odisha Distribution Limited, TP Northern Odisha Distribution Limited, TP Southern Odisha Distribution Limited, among others. It also supplies conductors, power cables to some of the private EPC players such as Montecarlo Limited, KRYFS Power Components Limited. Its diverse customer base also includes international clients which include government owned and controlled electricity companies, public enterprises and utilities, in Africa, Bangladesh, Bhutan and Nepal.

The company operates two key business segments namely: (i) Manufacturing; and (ii) EPC. As of March 31, 2026, it had 699 employees on its payroll and additional 1002 contract workers. As of the said date, it had an order book worth Rs. 324.34 cr. on hand.

The company is coming out with its maiden book building route secondary IPO of Rs. 742 cr. (approx. 34672897 equity shares of Rs. 5 each at the upper cap), The company has announced a price band of Rs. 203 – Rs. 214 per equity shares of Rs. 5 each. The IPO consists of fresh equity shares issue worth Rs. 542 cr. (approx. 25327103 equity shares at the upper cap), and an Offer for Sale (OFS) worth Rs. 200 cr. (approx. 9345794 equity shares at the upper cap). The issue opens for subscription on July 09, 2026, and will close on July 13, 2026. The minimum application to be made is for 70 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 24.70% of the post-IPO paid-up equity capital. From the net proceeds of the fresh equity issue, the company will spend Rs. 490.00 cr. for repayment/prepayment of certain borrowings, and the rest for general corporate purposes.

The company has allocated not more than 50% for QIBs, not less than 15% for HNIs, and not less than 35% for Retail investors.

The joint Book Running Lead Managers (BRLMs) to this issue are IIFL Capital Services Ltd., ICICI Securities Ltd., and MUFG Intime India Pvt. Ltd. is the registrar to the issue.

The company has issued initial equity shares at par value, and has issued further equity shares in the price range of Rs. 12.50 – Rs. 50.00 per share (based on FV of Rs. 5) between March 2001, and March 2022. It has also issued bonus shares in the ratio of 1 for 1 in February 2023, 8 for 1 in August 2025. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. NIL, Rs. 0.01, and Rs. 0.10, per share.

Post-IPO, its current paid-up equity capital of Rs. 57.52 cr. (115041240 equity shares) will stand enhanced to Rs. 70.18 cr. (140368343 equity shares). Based on the upper cap of the price band, the company is looking for a market cap of Rs. 3003.88 cr.

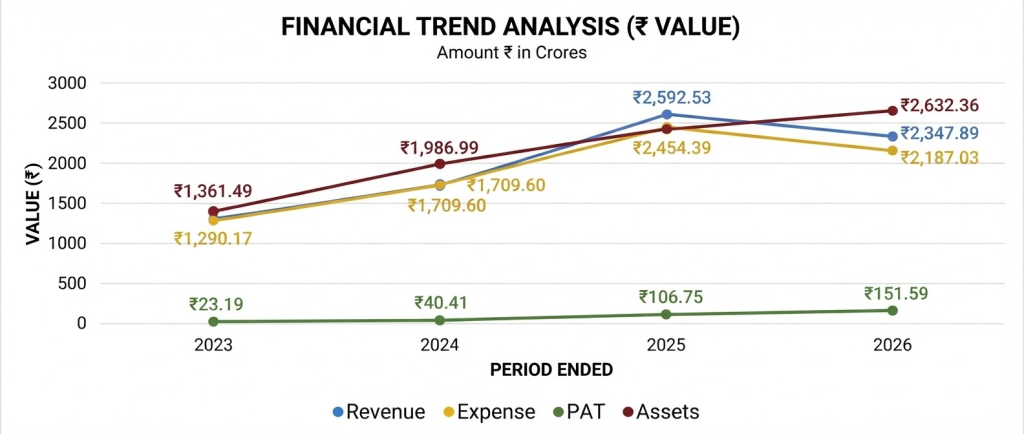

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted a total income/net profit, of Rs. 1763.65 cr. / Rs. 40.41 cr. (FY24), Rs. 2592.53 cr. / Rs. 106.75 cr. (FY25), and Rs. 2347.89 cr. / Rs. 151.18 cr. (FY26). The company posted inconsistency in its top lines for the reported periods. but continued to post surge in its bottom lines. It had a contingent liability of Rs. 26.78 cr. as of March 31, 2026. As of March 31, 2026, its debt/equity ratio of 1.10 raise concern.

According to the management, their backward integration with value added high margin products helped them sustaining gaining momentum in bottom lines for the reported periods. As they are paying off Rs. 490 cr. debt, it will bring savings on finance cost. They are gearing for high margin new products in coming years that will help them in sustaining the margins. It is a leader in north-east region for their products and their B2B segment play augurs well.

For the last three fiscals, the company has posted an average EPS of Rs. 10.17 and an average RoNW of 17.86 %. The issue is priced at a P/BV of 3.39 based on its NAV of Rs. 63.06 as of March 31, 2026, and at a P/BV of 2.37 based on its post-IPO NAV of Rs. 90.29 per share at the upper price.

If we attribute FY26 earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 19.81. Based on FY25 earnings, the P/E stands at 28.12. The issue appears fully priced.

For the reported periods, while the company has posted PAT margins of 2.29 % (FY24), 4.12% (FY25), 6.46% (FY26), and RoCE margins of 12.49%, 17.58%, 17.83%, respectively for the referred periods.

All amounts in Indian Rupees crores

The company not paid any dividends on equity shares for the reported periods of the offer document. It has already adopted a dividend policy in September 2025, based on its financial performance and future prospects. But it has paid dividends on Preference Shares for FY25 (Rs. 0.15) and for FY26 (Rs. 0.88) per share.

As per the offer document, the company has shown Apar Ind., Polycab India, KEI Ind., Dynamic Cables, Universal Cables, as its listed peers. They are currently trading at a P/E of 57.5, 57.4, 54.6, 21.2, and 24.3 (as of July 06, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

The two BRLMs associated with this issue have handled 76 issues in the last 3 fiscals (including the ongoing one), out of which 25 issues closed below the offer price on listing date.

LPIL is one of the leading players in power cables and conductors’ segment in North-East region. It sells its products on PAN India basis. The company improved its margins with backward integration and introduction of new high value/high margin products. The company is repaying around 59% debt, that will bring finance cost savings. Based on its recent financial data, the issue appears fully priced. Well-informed investors can park funds for medium to long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.