Horizon Reclaim IPO Review (BSE SME)

Horizon Reclaim (India) Ltd. (HRIL) is engaged in the manufacturing of reclaimed rubber, which is recycled rubber derived from used rubber materials such as old tyres, rubber tubes, tread peelings, and industrial scrap, including Ethylene Propylene Die ne Monomer (EPDM), a synthetic rubber known for its excellent resistance to heat. Reclaimed rubber serves as a cost-effective and environmentally friendly alternative to natural and synthetic rubber and is widely used in the manufacture of various rubber-based products.

The company offers reclaimed rubber in three main categories: (i) Natural Rubber Reclaim, produced from rubber tyre casings and tube commonly used in footwear soles, floor mats, tyre base layers, and moulded rubber products, (ii) Synthetic Rubber Reclaim, which includes EPDM and Butyl Reclaim Rubber suitable for applications requiring resistance to oil, heat, and weather, such as automotive seals, hoses, gaskets, and construction profiles and (iii) Crumb rubber made from recycle tyres and used in road construction, sport surfaces and construction materials like roofing sheets. Products are supplied in different grades depending on customer requirements.

To manufacture reclaimed rubber, HRIL relies on a steady supply of used rubber materials, sourced both domestically and through imports. Domestic sourcing is carried out through tyre dismantlers, waste collectors, and scrap dealers across various states in India. The principal raw materials include whole tyres (radial and tubeless), scrap tubes, scrap butyl tubes, scrap natural tubes, and other rubber scrap. By Sourcing from multiple locations, the company ensures regular availability of raw materials and supports uninterrupted production.

In addition, it has completed the construction and installation of plant and machinery at its manufacturing facility situate d at Bhagwanpur, Haridwar (Unit III). While the development of this facility has been completed, commercial operations at this unit are yet to commence. Further, it is in the process of establishing a manufacturing facility at Village Gundala, Rajkot, Gujarat (Unit II) to manufacture pyrolysis oil. The development of this unit is substantially completed, including construction of the necessary structures and installation of pyrolysis reactors. The company operates in B2B segment. Its debt-equity ratio of 1.44 as of March 2026, raise alarm. As of the said date, it had 81 employees on its payroll.

Issue Details / Capital History

The company is coming out with its maiden book building route IPO of 5269200 equity shares of Rs. 10 each to mobilize Rs. 54.27 cr. The company has announced a price band of Rs. 98 – Rs. 103 per share of Rs. 10 each). The minimum application to be made is for 2400 shares and in multiples of 1200 shares thereon, thereafter. The issue opens for subscription on June 12, 2026 and will close on June 16, 2026. The shares will be listed on BSE SME. The IPO constitute 27.00% of the post-IPO paid-up capital of the company. From the net proceeds of the issue, it will utilize Rs. 9.43 cr. for capex on installation of additional plant and machinery, Rs. 6.00 cr. for working capital, Rs. 26.70 cr. for repayment/prepayment of certain borrowing, sand the rest for general corporate purposes.

The IPO is solely lead managed by GYR Capital Advisors Pvt. Ltd., and KFin Technologies Ltd., is the registrar to the issue. Giriraj Stock Broking Pvt. Ltd., is the market maker.

After issuing entire initial equity capital at par value, the company issued bonus shares in the ratio of 18 for 1 in March 2025. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. 0.06, Rs. 0.24 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 14.25 cr. will stand enhanced to Rs. 19.52 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 201.01 cr.

IPO Lead Managers & Registrar

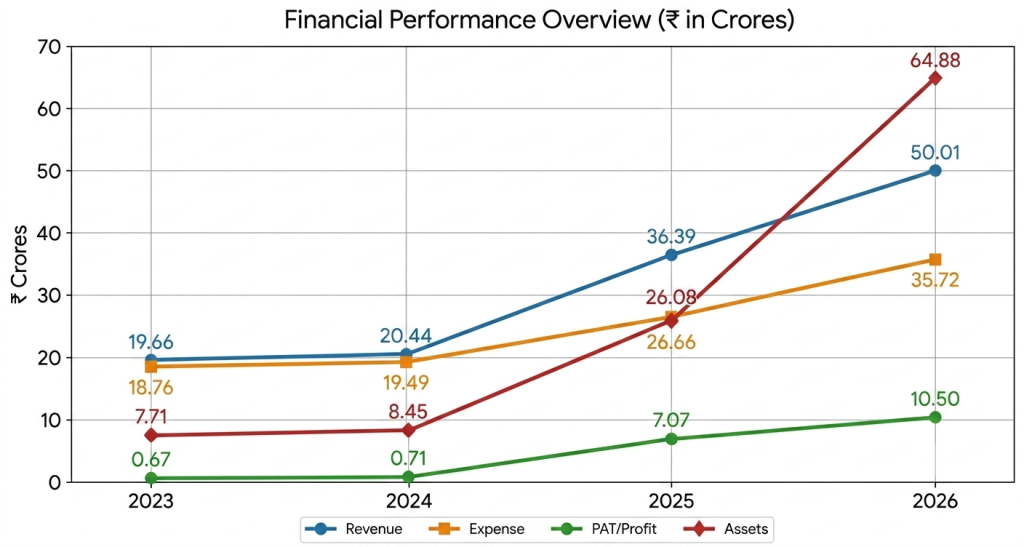

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted total income/ net profit, of Rs. 204.36 cr. / Rs. 0.71 cr. (FY24), Rs. 363.89 cr. / Rs. 7.07 cr. (FY25), Rs. 500.11 cr. / Rs. 10.50 cr. (FY26). The company marked growth in its top lines, but posted bumper profits from FY25 onwards, which not only raise concern, but also its sustainability going forward, as it is operating in a highly competitive and fragmented segment.

For the last three fiscals, the company has reported an average EPS of Rs. 5.42 and an average RoNW of 39.22%. The issue is priced at a P/BV of 5.91 based on its NAV of Rs. 17.43 per share as of MARCH 31, 2026, but its post IPO NAV data is missing from the offer documents.

If we attribute FY26 super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 19.14, and based on FY25 earnings, the P/E stands at 28.45. The issue appears aggressively priced based on its last three fiscals’ earnings.

The company has posted PAT Margins of 3.50% (FY24), 19.51% (FY25), 21.25% (FY26), and ROCE margins of 13.11%, 40.70%, 25.45%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has shown Lead Reclaim, as its listed peer. It is currently trading at a P/E of 16.6 (as of June 09, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears to be an eyewash.

Merchant Banker's Track Record

This is the 59th mandate from GYR Capital in the last six fiscals (including the ongoing one). Out of the last 11 listings, 2 listed at par, and the rest listed at premium ranging from 4.92% to 90.00% on the date of listing.

Conclusion

HRIL is engaged in the manufacturing of reclaimed rubber offering in three main categories in B2B segment. The company posted growth in its top and bottom lines for the reported periods. Sudden boost in its bottom lines, outperforming peers, raise eyebrows and concern over its sustainability. The company is operating in highly competitive and fragmented segment. Based on its recent financial data, the issue appears aggressively priced. Only well-informed/cash surplus investors may park funds for medium term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.