Happy Steels Ltd. (HSL) is an integrated manufacturer of Safety-Critical, Forged and Machined Transmission and Driveline components for On-highway vehicles, Off-highway vehicles, EV and Defence applications. Company’s product portfolio consists of wide range of Axles, Long Spline Shafts, Spindle and other related components that are critical of vehicle performance and safety. Over the years, the Company has developed strong capabilities in manufacturing safety-critical, high strength and load-bearing components through a combination of forging, precision machining, and stringent quality control processes that are supplied to original equipment manufacturers (“OEMs”) and Tier-I suppliers in India and overseas.

Its manufacturing operations are supported by an integrated process covering raw material procurement, forging, heat treatment, machining, gear cutting, drilling, surface hardening, grinding, inspection and packing. These capabilities enable it to manufacture components with defined mechanical properties, dimensional accuracy and consistency, in line with customer specifications. Since commencement of its commercial operations in 1996, the company has progressively scaled operations and achieved production volumes of 7,023.33 MT per annum of machines in cutting process, 6,268.33 MT per annum of machines in Forging Process and 4,597.13 MT per annum of machines in Machining Process during the Financial Year 2026.

HSL’s operations are engineering-driven and include capabilities such as reverse engineering of components, process design, validation and quality control. The company works closely with customers at various stages of the product lifecycle, including design finalization, process development and serial production. Its in-house facilities for forging, machining, heat treatment and testing allow it to maintain control over quality parameters and production timelines.

It has established long-term relationships with several customers, including OEMs and Tier-I suppliers, supported by its focus on consistent quality, timely delivery and ability to manufacture products across multiple specifications. Its customer base is diversified across domestic and export markets, reducing dependence on any single customer or vehicle segment. As of May 31, 2026, it had 403 employees on its payroll.

The company is coming out with its maiden book building route IPO of 3788000 equity shares of Rs. 10 each to mobilize Rs. 25.00 cr. at the upper cap. The company has announced a price band of Rs. 62 - Rs. 66 per share. The minimum application to be made is for 4000 shares and in multiples of 2000 shares thereon, thereafter. The IPO opens for subscription on July 09, 2026, and will close on July 13, 2026. The IPO constitute 26.52% of the post-IPO paid-up capital of the company. The shares will be listed on NSE SME Emerge. From the net proceeds of the IPO, it will utilize Rs. 13.16 cr. for capex on purchase of additional plant and machinery, Rs. 4.98 cr. for repayment/prepayment of loans., and the rest for general corporate purposes.

The IPO is jointly lead managed by Share India Capital Services Pvt. Ltd., and Master Capital Services Ltd., while Bigshare Services Pvt. Ltd., is the registrar to the issue. Share India Group’s Share India Securities Ltd., is the market maker.

After issuing entire initial equity capital at par value, the company issued bonus shares in the ratio of 6 for 1 in December 2025. The average cost of acquisition of shares by the promoters is Rs. 0.16, Rs. 0.28, Rs. 15.01, and Rs. 15.03 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 10.50 cr. will stand enhanced to Rs. 14.29 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 94.29 cr.

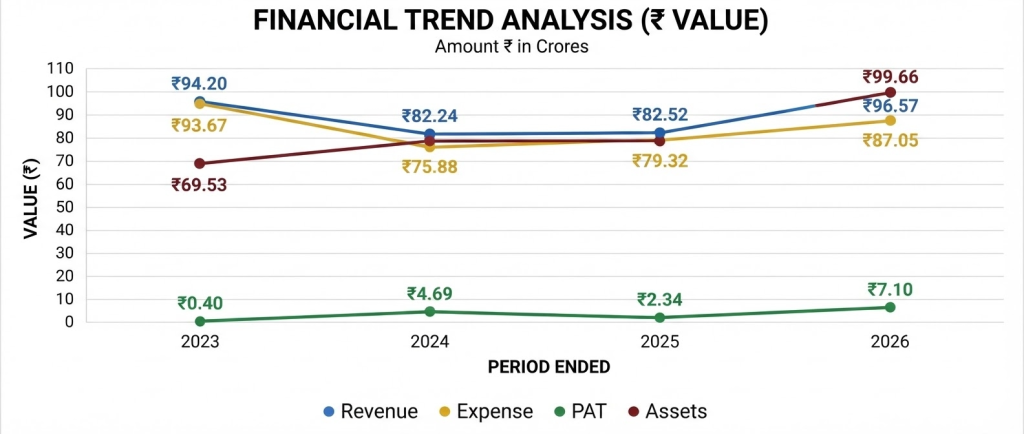

On the financial performance front, for the last three fiscals, the company has reported a total income/net profit of Rs. 82.24 cr. / Rs. 4.69 cr. (FY24), Rs. 82.52 cr. / Rs. 2.34 cr. (FY25), Rs. 96.57 cr. / Rs. 7.10 cr. (FY26). While it posted inconsistency in its bottom lines for FY24 and FY25 despite static top line, the downtrend for FY25 raise concern. It FY26 it posted growth that appears to be a window dressing to fetch fancy valuation for the IPO. Its contingent liability of Rs. 4.03 cr. as of March 31, 2026, raise alarm. Its debt-equity ratio of 1.18 as of March 31, 2026 raise concern.

For the reported period, the company has reported an average EPS of Rs. 4.87, and an average RoNW of 13.81%. The issue is priced at a P/BV of 1.73 based on its NAV of Rs. 38.09 per share as of March 31, 2026, but its post-IPO NAV data is missing from the offer documents.

If we attribute FY26 super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 13.28, and based on FY25 earnings, the P/E stands at 40.24. The issue appears aggressively priced.

For the reported periods, the company has posted PAT margins of 2.52% (FY24), 6.44% (FY25), 9.12% (9M-FY26), and RoCE margins of 27.51%, 73.66%, 46.48%, respectively, for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividend for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown EMM Force, Kross Ltd., GNA Axles, as its listed peers. They are currently trading at a P/E of 45.4, 21.3, and 17.3 (as of July 06, 2026. However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

This is the 21st mandate from Share India Capital in the last four fiscals (including the ongoing one). From the last 10 listings, 4 listed at discount, 1 at par and the rest with premium ranging from 23.33% to 90.00 % on the listing date.

HSL is engaged in the manufacturing and marketing of safety-critical, forged and machined transmission and driveline components for on/off highway vehicles, EVs etc. The company posted inconsistency in its bottom lines for the reported periods. It is operating in a highly competitive and fragmented segment. Based on its recent financial data, the issue appears aggressively priced. Ony well-informed/risk seekers/cash surplus investors may park moderate funds for medium term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.