Powerica Ltd. (PL) is an integrated power solutions provider specializing in diesel generator sets (“DG sets”), for both primary and standby applications. As one of the original equipment manufacturers (“OEMs”) for Cummins India Limited (“Cummins India”, along with its affiliates, “Cummins”), it has maintained a relationship with them for over four decades.

PL commenced its DG sets business in 1984, and subsequently expanded generator set portfolio to include medium speed large generators (“MSLG”) in 1996. The company continues to develop this segment through a collaboration with HD Hyundai Heavy Industries Co., Limited (“Hyundai”), on a non-exclusive basis. By integrating its DG set and MSLG offerings, it provides a comprehensive range of generator sets with capacities ranging from 7.5 kVA to 10,000 kVA, designed to meet the distinctive requirements of diverse industries and applications. As of the date of this Red Herring Prospectus, its generator set business comprises of DG sets powered by Cummins engines, MSLG offerings in collaboration with Hyundai, and certain allied business activities (“Generator Set Business”).Building on its experience in the Generator Set Business, the company entered the wind power sector in 2008 as an independent power producer (“IPP”). Subsequently, it developed capabilities as an engineering, procurement and construction (“EPC”) contractor as well as an operation and maintenance (“O&M”) service provider for balance of plant (“BoP”). As of the date of this Red Herring Prospectus, its operations in the wind power sector includes developing and operating IPP projects as well as undertaking EPC and O&M activities for BoP primarily within the wind power industry (“Wind Power Business”).

PL manufactures DG sets along with auxiliary items, including acoustic enclosures, fuel and exhaust systems, and customized control panel systems. Its offering comprises of comprehensive high speed generator solutions, powered by Cummins engines, covering the design, marketing, manufacturing, testing, supply, installing, and commissioning of DG sets ranging from 7.5 kVA to 3,750 kVA. According to the F&S Report, based on capacity, DG sets are broadly classified as low horse power with a range of 7.5 kVA to 160 kVA (“LHP”), medium horse power with a range of 180 kVA to 500 kVA (“MHP”) and high horse power with a range above 500 kVA (“HHP”).Since inception in 1984, the company has formed a long standing relationship with Cummins, as one of their OEMs. The engines and alternators for its DG sets are sourced directly from Cummins. It has entered into a non-exclusive general supply agreement dated June 11, 2025 (“General Supply Agreement”),

with Cummins India. According to the F&S Report, in Fiscal 2025, Cummins India was one of the leading engine manufacturers in both, the MHP and HHP ranges of DG sets in India. It also collaborates with Cummins on the integration and testing of diesel generator products, ensuring alignment with evolving technological, regulatory, environmental and emission standards. PL operates in-house manufacturing facilities to maintain direct control over processes, costs, and timelines. As of the date of this Red Herring Prospectus, the company owns and operates three manufacturing facilities located in Bengaluru, Karnataka; Silvassa, Dadra and Nagar Haveli; and Khopoli, Maharashtra. Its captive manufacturing approach enables it to optimize inventory, uphold quality assurance standards, and manage supply chain costs and delivery timelines. This structure also enhances its responsiveness to changing customer needs and facilitates faster time-to-market. Its extensive sales network supports effective customer engagement and market penetration.

The company is coming out with its maiden book building route combo IPO worth Rs. 1100 cr. (approx. 27848101 equity shares of Rs. 5 each at the upper cap). The IPO consists of fresh equity shares issue worth Rs. 700 cr. (approx. 17721519 equity shares at the upper cap), and an Offer for Sale (OFS) worth Rs. 400 cr. (approx. 10126582 equity shares at the upper cap). The company has announced a price band of Rs. 375 – Rs. 395 per equity shares of Rs. 5 each. The issue opens for subscription on March 24, 2026, and will close on March 27, 2026. The minimum application to be made is for 37 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 22.01% of the post-IPO paid-up equity capital. From the net proceeds of fresh equity issue, the company will utilize Rs. 525 cr. for repayment/prepayment of certain borrowings, and the rest for general corporate purposes.

The company has reserved equity shares worth Rs. 2.00 cr. (approx. 50633 equity shares at the upper cap), and offering them a discount of Rs. 37 per share. From the rest, it has allocated not more than 50% for QIBs, not less than 15% for HNIs and not less than 35% for Retail investors.The joint Book Running Lead Managers (BRLMs) to this issue are ICICI Securities Ltd., IIFL Capital Services Ltd., Nuvama Wealth Management Ltd., while MUFG Intime India Pvt. Ltd., is the registrar to the issue. Nuvama Wealth Management Ltd. is also a syndicate member.

After issuing initial equity shares at par, the company has issued/converted further equity shares at the price of Rs. 1634.495 (based on Rs. 5 FV) in October 2007. It has also issued bonus shares in the ratio of 6 for 1 in January 1993, 6 for 1 in September 1993, 4 for 5 in February 2011, 3 for 2 in June 2018, and 3 for 1 in June 2025. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. NIL per share.

After issuing initial equity shares at par, the company has issued/converted further equity shares at the price of Rs. 1634.495 (based on Rs. 5 FV) in October 2007. It has also issued bonus shares in the ratio of 6 for 1 in January 1993, 6 for 1 in September 1993, 4 for 5 in February 2011, 3 for 2 in June 2018, and 3 for 1 in June 2025. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. NIL per share. Post-IPO, its current paid-up equity capital of Rs. 54.41 cr. will stand enhanced to Rs. 63.27 cr. Based on the upper cap of the IPO price band; the company is looking for a market cap of Rs. 4998.60 cr.

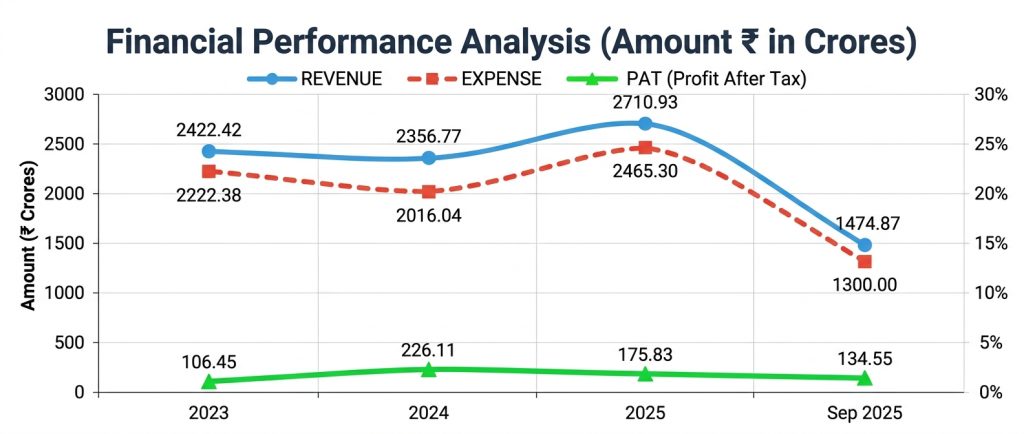

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted a total income/net profit, of Rs. 2422.42 cr. / Rs. 106.45 cr. (FY23), Rs. 2356.77 cr. / Rs. 226.11 cr. (FY24), and Rs. 2710.93 cr. / Rs. 175.83 cr. (FY25). For H1 of FY26 ended on September 30, 2025, it earned a net profit of Rs. 134.55 cr. on a total income of Rs. 1474.87 cr.

For the last three fiscals, the company has posted an average EPS of Rs. 14.84 and an average RoNW of 18.18 %. The issue is priced at a P/BV of 3.54 based on its NAV of Rs. 111.60 as of September 30, 2025, and at a P/BV of 4.12 based on its post-IPO NAV of Rs. 95.97 per share (at the upper cap).

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 18.58. Based on FY25 earnings, the P/E stands at 28.44. Thus, the issue appears reasonably priced.

For the reported periods, the company has posted PAT margins of 4.39% (FY23), 9.59% (FY24), 6.49% (FY25), 9.12% (H1-FY26), and RoCE margins of NA, 43.47%, 27.02%, 13.90% respectively, for reported periods.

The company has not paid any dividends for the reported periods of the offer document, except an interim dividend of 55% in March 2026. It has already adopted a dividend policy in June 2025, based on its financial performance and future prospects.

As per the offer document, the company has shown Cummins India, Kirloskar Oil, NTPC Green, Acme Solar, Adani Green, as its listed peers. They are currently trading at a P/E of 53.6, 37.9, 149.0, 31.7, and 85.4 (as of March 19, 2026). However, they are not truly comparable on an apple-to-apple basis.

The three BRLMs associated with this issue have handled 127 public issues in the past three years, out of which 38 issues closed below the offer price on listing date.

PL is engaged in providing integrated power solutions and specializes in DG Sets. It has also ventured in to wind power generation and has running projects in Gujarat. The company reported inconsistency in its top and bottom lines for the reported periods. It is operating in a highly competitive and fragmented segment. Based on its recent financial data, the issue appears reasonably priced. Well-informed investors can park funds for medium to long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.