Advit Jewel IPO Review

Advit Jewels Ltd. (AJL) is a manufacturer and seller of traditional and contemporary handcrafted fine jewellery, specializing in Kundan, Polki, Diamond and Studded pieces. Its brand name “Rambhajo” finds its roots in a jewellery business established in 1921in Jaipur, the heart of India's gemstone and jewellery hub. The brand name evolved steadily into a well-known brand in the jewellery manufacturing and retail space in Jaipur, Rajasthan. In order to carry on the business in a corporate structure, the Company was incorporated as a private limited Company in the year in 2019, to carry forward the legacy of Rambhajo brand and its craftmanship spanning more than 100 years. Along with the experience of its promoters, it continues to uphold the tradition of fine jewellery while operating under the brand “Rambhajo since 1921”.

With its expertise in craftsmanship and a keen understanding of changing customer tastes, the company blends traditional methods with contemporary designs to create jewellery that feels both timeless and relevant. Its pieces are crafted using handmade techniques, but it also incorporates modern design elements, ensuring each item is not only beautiful but also reflects a rich cultural heritage. The result is jewellery that is elegant, meaningful and appeals to both classic and modern sensibilities.

Its core strength lies in design innovation and customization, offering clients the flexibility to tailor jewellery according to specific tastes, cultural significances and market trends. From bridal collections to everyday luxury pieces, its offerings cater to a diverse clientele across Indian markets. With a commitment to quality, authenticity and customer satisfaction, it ensures that each piece it creates reflects meticulous craftsmanship, carefully sourced materials and a deep understanding of heritage artistry. AJL’s offerings include necklaces, earrings, rings, bangles and customized jewellery pieces. it works primarily with gold, diamond polki, and coloured stones and are known for its work in Kundan and Polki. Kundan Polki Jewellery is renowned for its intricate craftsmanship and timeless elegance. This traditional technique, which combines the artistry of setting uncut diamonds with detailed gold work, is labour intensive but produces unique and exquisite pieces.

The company does innovation and designing every day by blending different art forms from different locations in the world. Its every design is unique and is not repeated. Its products are designed in both 14 Carat and 18 Carat gold depending on customer preferences. It largely operates on a B2B model, serving dealers, showrooms and jewellery retailers. At the same time, it also caters to B2C customers for exclusive, made-to-order pieces.

AJL’s jewellery is a 100% handmade jewellery. its artisans are also trained since generations to create jewellery that it manufactures. Its forte of blending artwork is only possible due to these skillful artisans who know how to amalgamate different art forms following its aesthetical designs.

As of December 31, 2025, it had 196 customers and marketed 10 products. The total employee tally stood at 111 as of April 30, 2026. The capacity utilization was at 21.58% for the period ended December 31, 2025.

MAJOR POINTS OF ALERT:

The company claims to be the only well established player in Polki/Kundan jewellery that has good demand in rich family’s marriage ceremonies. Their products are antic and traditional piece of art and enjoys preferences. However, the company is catering to B2B segment (around 80%%) and for B2C (around 20%%). But in the given scenario of appeal by Prime Minister to avoid un-necessary buying of Gold on one hand and hike in import duty of Gold on the other, this segment is currently witnessing lower demand. This announcement has dampened sentiment for the gold jewellery segment for a while. Its outperforming margins amidst peers raise concern as it may not be able to sustain the same. However, the management is confident of sustaining its volume as well as margins.

Issue Details / Capital History

The company is coming out with its maiden book building route primary IPO of 11968000 equity shares of Rs. 10 each to mobilize Rs. 165.16 cr. at the upper cap. The company has announced a price band of Rs. 130 – Rs. 138 per equity shares of Rs. 10 each. The issue opens for subscription on June 23, 2026, and will close on June 25, 2026. The minimum application to be made is for 100 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 26.13% of the post-IPO paid-up equity capital. From the net proceeds of the IPO, the company will utilize Rs. 65.00 cr. for working capital, Rs. 65.00 cr. for repayment/prepayment of certain outstanding borrowings, and the rest for general corporate purposes.

The company did pre-IPO placement of 1832000 equity shares at a price of Rs. 125 per share and mobilized Rs. 22.90 cr., which has been utilized for objects of the issue disclosed in the offer document. The IPO size is reduced to the extent of pre-IPO placement amount.

The sole Book Running Lead Manager (BRLM) to this issue is Holani Consultants Pvt. Ltd., and Bigshare Services Pvt. Ltd., is the registrar to the issue. Holani Consultants Pvt. Ltd. is also a syndicate member.

The company has issued initial equity shares at par value, and there after did a pre-IPO placement of 1832000 equity shares at Rs. 125 per share in May 2026. It has also issued bonus shares in the ratio of 3200 for 1 in August 2025. The average cost of acquisition of shares by the promoters is Rs. NIL per share.

Post-IPO, its current paid-up equity capital of Rs. 33.84 cr. will stand enhanced to Rs. 45.81 cr. Based on the upper cap of the price band, the company is looking for a market cap of Rs. 632.18 cr.

IPO Lead Managers & Registrar

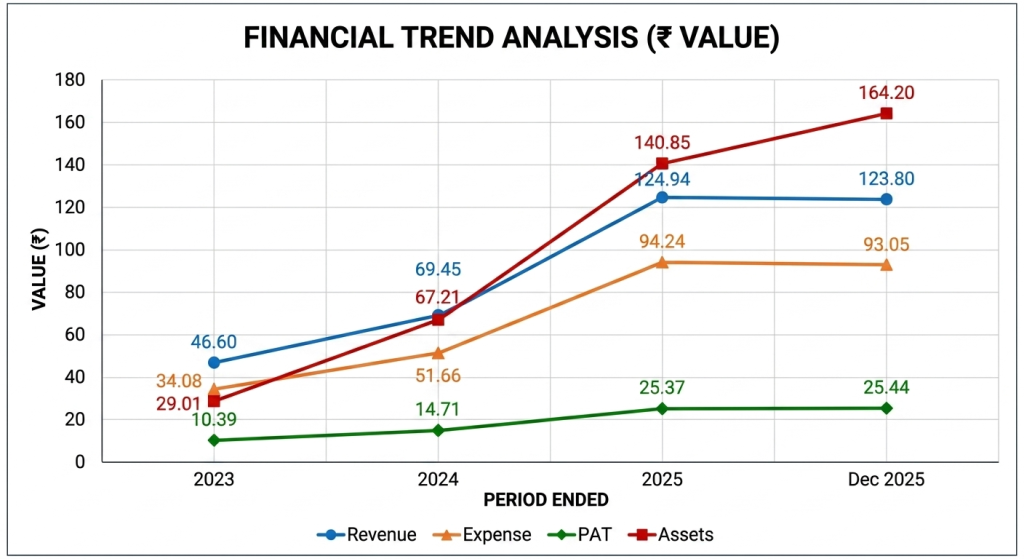

On the financial performance front, for the last three fiscals, the company has posted a total income/net profit, of Rs. 46.60 cr. / Rs. 10.39 cr. (FY23), Rs. 69.45 cr. / Rs. 14.71 cr. (FY24), and Rs. 124.94 cr. / Rs. 25.37 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 25.44 cr. on a total income of Rs. 123.80 cr. The company posted growth in its top and bottom lines for the reported periods.

For the last three fiscals, the company has posted an average EPS of Rs. 6.04 and an average RoNW of 46.34 %. The issue is priced at a P/BV of 5.28 based on its NAV of Rs. 26.13 as of December 31, 2025, and at a P/BV of 2.33 based on its post-IPO NAV of Rs. 59.31 per share at the upper cap.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 18.62. Based on FY25 earnings, the P/E stands at 24.91. The issue appears aggressively priced despite recent super financial data.

For the reported periods, while the company has posted PAT margins of 22.29% (FY23), 21.18 % (FY24), 20.30% (FY25), 20.55% (9M-FY26), and RoCE margins of 53.02%, 35.41%, 27.48%, 24.09%, respectively for the referred periods.

All amounts in Indian Rupees crores

The company not paid any dividends for the reported periods of the offer document. It has already adopted a dividend policy in September 2025, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has shown Bluestone Jewellery, RBZ Jewellers, Radhika Jeweltech, as its listed peers. They are currently trading at a P/E of 517.0, 9.69, and 9.03 (as of June 18, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

Merchant Banker's Track Record

The sole BRLM associated with this issue has handled 6 issues in the last 3 fiscals (including the ongoing one), out of which no issues closed below the offer price on listing date.

Conclusion

AJL is manufacturer and seller of traditional and contemporary handcrafted jewellery. It specialized in Kundan, Polki, Diamond and studded pieces. The company posted growth in its top and bottom lines for the reported periods. Based on its recent financial data, the issue appears aggressively priced. Only well-informed/cash surplus/risk seeker investors may park moderate funds for long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.

One Response

Good company.welnon to me every invester can invest without any hesitation