Kratikal Tech Ltd. (KTL) is engaged in providing AI-driven, Software-as-a-Service–based cybersecurity solutions through its proprietary security software platform, supported by cybersecurity and regulatory compliance services, enabling enterprises to achieve measurable cyber risk reduction and enhanced resilience. Its People Security Management (PSM) capabilities are delivered through the proprietary Threatcop platform, which focuses on reducing human-related cyber risks, and are enhanced by technology and process security offerings delivered under the Kratikal brand.

Together, these offerings provide integrated protection across the People–Process–Technology stack, supporting organizations in proactively identifying, prioritizing, and mitigating cyber risks while strengthening their overall security posture in an increasingly threat environment. Through its services, the company empower organizations to protect their critical data, prevent cyber threats, and ensure smooth business operations. KTL’s solutions are designed to eliminate data privacy risks, safeguarding businesses from unauthorized access and security breaches.

The company operates through two integrated business i.e., AI Driven People Security Management, and Technology and Process Security Services. In its services portfolio, the Company has developed Threatcop, a people security management suite and AutoSecT, an AI-driven pentest and VMDR platform. AutoSecT autonomously scans network, cloud, web, mobile, and API assets, prioritizes vulnerabilities based on risk, and provides AI-driven patch recommendations, supported by analytics dashboards for security teams and a dedicated CISO dashboard.

The platform standardizes and enables the delivery of all penetration testing reports undertaken by the Company, enhancing scalability, consistency, and turnaround time, while embedding the Company’s intellectual property at the core of its service offerings. The Company has undertaken AI driven VMDR, secure code reviews, and vulnerability assessments across diverse customer. As of March 31, 2026, it had 200 employees on its payroll.

The company is coming out with its maiden book building route IPO of 2940000 equity shares of Rs. 10 each to mobilize Rs. 39.69 cr. The company has announced the price band of Rs. 128 – Rs. 135 per share. The minimum application to be made is for 2000 shares and in multiples of 1000 shares thereon, thereafter. The issue opens for subscription on June 30, 2026 and will close on July 02, 2026. The shares will be listed on BSE SME. The IPO constitute 26.49% of the post-IPO paid-up capital of the company. From the net proceeds of the issue, the company will utilize Rs. 23.08 cr. for investment in its subsidiaries Threatcop LLC, KUAE, USA, Rs. 9.23 cr. for investment in product development, and the rest for general corporate purposes.

The IPO is solely lead managed by Beeline Capital Advisors Pvt. Ltd., and KFin Technologies Ltd. is the registrar to the issue. Beeline group’s Spread X Securities Pvt. Ltd. is a market maker, as well as syndicate member.

After issuing initial equity capital at par value, the company issued further equity shares in the price range of Rs. 100 – Rs. 20000 per share between May 2017, and December 2025. It also issued bonus shares in the ratio of 600 for 1 in November 2025. The average cost of acquisition of shares by the promoters is Rs. 1.08, Rs. 2.31, and Rs. 9.92 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 8.16 cr. will stand enhanced to Rs. 11.10 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 149.86 cr.

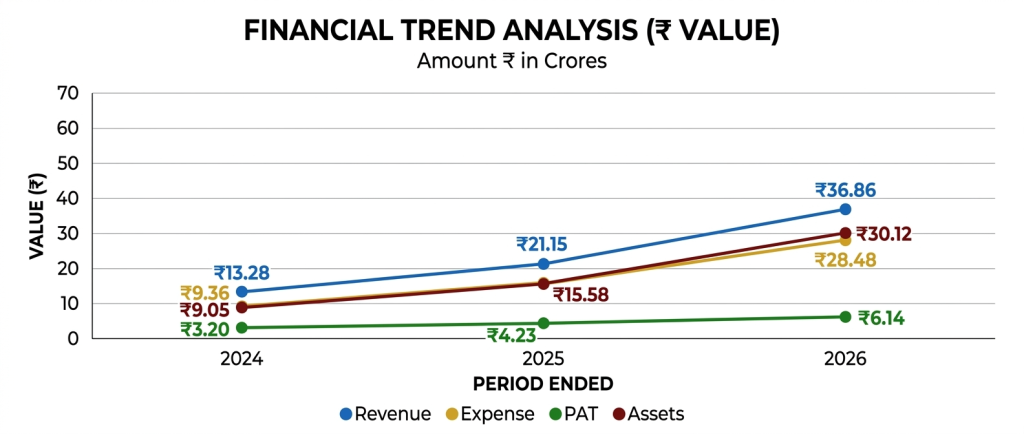

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted total income/ net profit, of Rs. 13.28 cr. / Rs. 3.20 cr. (FY24), Rs. 21.15 cr. / Rs. 3.81 cr. (FY25), Rs. 36.86 cr. / Rs. 6.14 cr. (FY26). The company marked super growth in its top and bottom lines for the reported periods. According to the management, their heck and fraud arresting IT solutions are catching attention and are flooded with orders. For FY26, it posted 29.94% exports revenue and 70.06% domestic against 13.05% and 86.95% for FY24. Thus, the company is posting growth in its exports earnings and the trends will continue. Top 10 customers contribute 31.60% of its top line for FY26.

For the last three fiscals, the company has reported an average EPS of Rs. 6.85 (basic) and an average RoNW of 32.35%. The issue is priced at a P/BV of 4.59 based on its NAV of Rs. 29.43 per share as of March 31, 2026, but its post IPO NAV data is missing from the offer documents.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 24.41, and based on FY25 earnings, the P/E stands at 39.24. The issue appears fully priced based on its recent earnings.

The company has posted PAT Margins of 24.61% (FY24), 18.29% (FY25), 16.73% (FY26), and ROCE margins of 56.30%, 47.48%, 34.35%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown AAA Technologies, Accedere Ltd., as its listed peers. They are currently trading at a P/E of 59.2 and 53.4 (as of June 25, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears as an eyewash.

This is the 72nd mandate from Beeline Capital in the last five fiscals (including the ongoing one). Out of the last 15 listings, 4 opened at discount, 1 at par and the rest with premium ranging from 1.28% to 146.91% on the date of listing.

KTL is engaged in providing AI-driven SaaS based cybersecurity solutions. It marked speedy growth in its operations for the reported period of RHP. Its export revenue grew from 13.05% for FY24 to 29.94% for FY26. Based on its recent financial data, the issue is fully priced. Well-informed investors may park funds for medium to long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.