Sampark India Logistic Ltd. (SILL) operates as a carrying and forwarding agent, offering comprehensive logistics solutions that cover the entire supply chain, from the point of origin to the final point of destination, ensuring the company meets the diverse needs of customers and clients. As a Pan-India logistics provider operating through a network of 50 branch offices as on the date of this Red Herring Prospectus, it delivers integrated services, including freight forwarding and warehousing to clients across various industries such as automotive, pharma, consumer durables, textiles, pharma and more.

Since its inception in 2012, it is operating under B2B segment which require transporting bulk quantities of clients’ goods from one place to another within India. The Company has ISO Certification 9001:2015 for Quality Management System and ISO Certification 45001:2018 for Occupational Health and Safety Management Systems for supply chain solutions- logistics services by Air/Train/Surface/Sea and Warehousing services. It operates primarily from its registered office situated in Delhi and corporate office situated in Haryana.

As on the date of Red Herring Prospectus, it operates a fleet of 56 commercial vehicles that are owned by it. The company provides both FTL (Full Truckload) and LTL (Less Than Truckload) services based on clients’ needs. FTL refers to a shipping method where a single shipment fills the entire capacity of a truck. This is typically used when a business needs to move enough goods to fill a truck or prefers exclusive use of a truck for a particular shipment. FTL is commonly utilized in industries such as manufacturing and retail, where large volumes of goods need to be transported securely and efficiently.

On the other hand, LTL involves consolidating shipments from various customers into one truck, with each shipment occupying only part of the truck's space. This method allows businesses to share transportation costs making it a cost effective and efficient option for those who don't require a full truckload.

Further, as on the date of this RHP, it operates a total of 8 warehouses comprising of 1,24,500 square feet, which are taken on lease and directly managed by the company, located in Ambala, Roorkee, Hyderabad, Aurangabad, Chennai, Bangalore, Nashik and Bhiwandi. Its warehousing services include inventory management, storage management and packaging of goods. As of April 30, 2026, it had 344 employees on its payroll.

The company is coming out with its maiden book building route IPO of 3240000 equity shares of Rs. 10 each to mobilize Rs. 27.22 cr. The company has announced the price band of Rs. 80 – Rs. 84 per share. The minimum application to be made is for 3200 shares and in multiples of 1600 shares thereon, thereafter. The issue opens for subscription on June 30, 2026 and will close on July 02, 2026. The shares will be listed on BSE SME. The IPO constitute 26.43% of the post-IPO paid-up capital of the company. From the net proceeds of the issue, the company will utilize Rs. 19.72 cr. for working capital, and the rest for general corporate purposes.

The IPO is solely lead managed by Finshore Management Services Ltd., and Maashitla Securities Pvt. Ltd. is the registrar to the issue. Rikhav Securities Ltd. is a market maker, and also a syndicate member. The IPO is underwritten to the tune of 15% by Finshore Management, and 85% by Srujan Alpha Capital.

After issuing entire initial equity capital at par value, the company issued bonus shares in the ratio of 2 for 1 in June 2024. The average cost of acquisition of shares by the promoters is Rs. 3.33, and Rs. 4.34 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 9.02 cr. will stand enhanced to Rs. 12.26 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 102.97 cr.

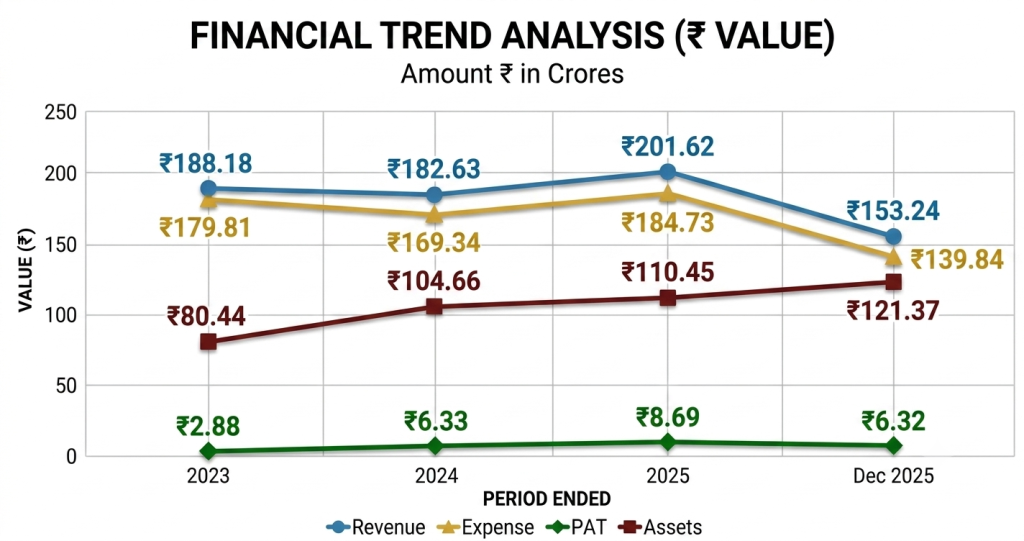

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 188.18 cr. / Rs. 3.28 cr. (FY23), Rs. 182.63 cr. / Rs. 6.37 cr. (FY24), Rs. 201.62 cr. / Rs. 8.76 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 6.32 cr. on a total income of Rs. 153.24 cr. Though the company marked decline in its top line for FY24, its bottom line improved. Thereafter, it continued to post super margins. According to the management, its all related service offerings under one roof has improved their capabilities as well as margins. It is adhering to its IT enabled operations that not only eases its process, but also helps improving its margins.

For the last three fiscals, the company has reported an average EPS of Rs. 7.01 and an average RoNW of 21.44%. The issue is priced at a P/BV of 1.72 based on its NAV of Rs. 48.71 per share as of December 31, 2025, but its post IPO NAV data is missing from the offer documents.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 12.21, and based on FY25 earnings, the P/E stands at 11.76. The issue appears fully priced based on its recent earnings.

The company has posted PAT Margins of 1.74% (FY23), 3.51% (FY24), 4.36% (FY25), 4.14% (9M-FY26), and ROCE margins of 22.04%, 30.93%, 33.54%, 21.01%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown Orissa Bengal Carrier, GB Logistics, VRL Logistics as its listed peers. They are currently trading at a P/E of NA, 2.82, and 17.7 (as of June 25, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears as an eyewash.

This is the 34th mandate from Finshore Management in the last five fiscals (including the ongoing one). Out of the last 10 listings, 6 opened at discount, 1 at par and the rest with premium ranging from 0.64% to 9.09% on the date of listing. The merchant banker has a poor track record.

SILL operates as a carrying and forwarding agent and provides services on a B2B model. It offers all related services under one roof with IT enable mode that helps them improving its operations and improve margins. It offers FTL, LTL, truck load services as per the demands from its customers. It operates on a PAN India basis and providing end to end services. Based on its recent financial data, the issue appears fully priced. Well-informed/cash surplus investors may park moderate funds for long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.