Atharva Polyplast Ltd. (APL) is a manufacturer of precision plastic components with a growing presence across key industrial verticals including furniture, home appliances, and automotive assemblies. Its focus is on injection moulded components, primarily made from polypropylene (PP), ABS, HDPE, and engineering polymers. The company supports both B2B manufacturing contracts and co-development projects, providing full-cycle support from mould design and prototyping to final production and QA validation.

The Company uses its moulding capabilities and know-how to supply customized plastic components to OEMs and Tier-1 suppliers in India. As part of its engagements with OEM customers, the company converts raw materials and bought-out parts such as fasteners, hinges or foam components into plastic components based on the customer’s needs.

Its manufacturing facility spread over 2,34,614 Sq. Ft. was commissioned in the year 2015 and has a production space of 40,000 Sq. Ft. The facility is equipped with over 17 moulding machines with capacities ranging from 100T to 1000T, enabling the manufacturing of plastic components used in industries such as furniture, home appliances, automotive, and others.

It has an in-house quality control room and a qualified team that monitors the entire production cycle from the procurement of raw materials to the final inspection of finished products. APL’s quality management systems are certified under ISO 9001:2015 (Quality Management), ISO 14001:2015 (Environmental Management), and ISO 45001:2018 (Occupational Health & Safety). In addition, its facility has undergone a SMETA (Sedex Members Ethical Trade Audit) which covered Labour Standards; Health and Safety; Environment 4-Pillar; and Business ethics. The audit concluded that APL’s facility maintains an overall ‘robust management system’, while also identifying certain areas for improvement, in line with its efforts to maintain responsible business practices and continuously enhance workplace standards. As of May 06, 2026, it had 41 employees on its payroll, and is also hiring contract workers as and when needed.

The company is coming out with its maiden book building route IPO of 4500000 equity shares of Rs. 10 each to mobilize Rs. 27.00 cr. The company has announced the price band of Rs. 55 – Rs. 60 per share. The minimum application to be made is for 4000 shares and in multiples of 2000 shares thereon, thereafter. The issue opens for subscription on June 30, 2026 and will close on July 02, 2026. The shares will be listed on BSE SME. The IPO constitute 26.71% of the post-IPO paid-up capital of the company. From the net proceeds of the issue, the company will utilize Rs. 13.00 cr. for working capital, Rs. 3.00 cr. for capex for purchase of machineries, Rs. 3.00 cr. for repayment/prepayment of certain borrowings, and the rest for general corporate purposes.

The IPO is solely lead managed by Horizon Management Pvt. Ltd., and MUFG Intime India Pvt. Ltd. is the registrar to the issue. R K Stockholding Pvt. Ltd. is a market maker. The issue is underwritten to the tune of 15.02% by Horizon Management, and 84.98% by R K Stockholding.

After issuing/converting entire initial equity capital at par value, the company issued bonus shares in the ratio of 9 for 10 in July 2025. The average cost of acquisition of shares by the promoters is Rs. 2.23, and Rs. 4.19 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 12.35 cr. will stand enhanced to Rs. 16.85 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 101.10 cr.

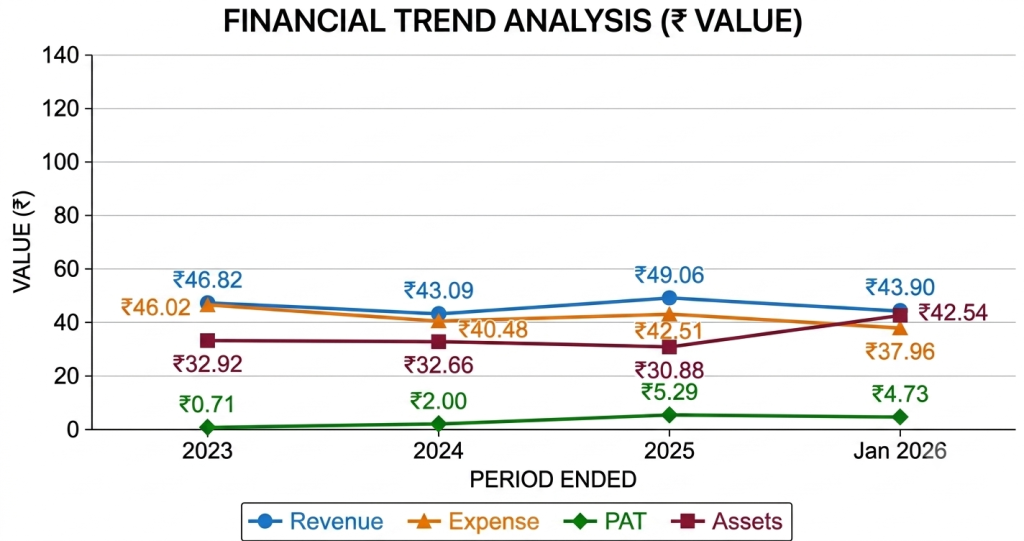

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 46.82 cr. / Rs. 0.71 cr. (FY23), Rs. 43.09 cr. / Rs. 2.00 cr. (FY24), Rs. 49.06 cr. / Rs. 5.29 cr. (FY25). For 10M of FY26 ended on January 31, 2026, it earned a net profit of Rs. 4.73 cr. on a total income of Rs. 43.90 cr. Though the company marked decline in its top line for FY24, its bottom line improved. Thereafter, it continued to post super margins. For this, the management clarified that due to shift in its products that had high margin, though its top line marked marginal growth, its bottom line got boosted. This trend will continue as the company has shifted its focus on such business.

For the last three fiscals, the company has reported an average EPS of Rs. 2.78 and an average RoNW of 31.03%. The issue is priced at a P/BV of 5.70 based on its NAV of Rs. 10.53 per share as of March 31, 2025, but its post IPO NAV data is missing from the offer documents. The company could have given its NAV as of January 31, 2026.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 17.86, and based on FY25 earnings, the P/E stands at 19.11. The issue appears fully priced based on its recent earnings.

The company has posted PAT Margins of 1.58% (FY23), 4.82% (FY24), 11.12% (FY25), 11.14% (10M-FY26), and ROCE margins of 12.58%, 18.94%, 35.31%, 24.92%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown Master Components as its listed peer. It is currently trading at a P/E of 18.6 (as of June 25, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears as an eyewash.

This is the 27th mandate from Horizon Management in the last four fiscals (including the ongoing one). Out of the last 10 listings, 4 opened at discount, 1 at par and the rest with premium ranging from 3.08% to 90.00% on the date of listing.

APL is engaged in the manufacturing of precision plastic components for user across industry. It largely operates on B2B model and has good relationship with many renowned OEMs. It posted de-growth in its top line for FY24, but posted higher margins following shift of its product mix. Based on its recent financial data, the issue appears fully priced. Well-informed investors may park funds for medium to long term

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.