Anubhav Plast Ltd. (APL) is engaged in the business of manufacturing of Electric Resistance Welding (“ERW”) Steel Pipes & Tubes in round and square hollow sections/shapes and swaged steel tubular poles in India, with operations spanning more than three decades. Under the “ANUBHAV” brand, it manufactures ERW steel pipes, tubes, and hollow sections that bear the ISI certification mark at every meter, reflecting its unwavering commitment to quality. These products are used across a wide range of sectors including electricity transmission and distribution, street lighting, telecom infrastructure, construction, irrigation, water supply, general engineering, and fabrication. APL’s ERW products are manufactured in compliance with IS:2713, IS:9295, IS:1239, IS:4270, IS:1161, IS:4923, and IS:3589, and are widely accepted by its valued customers for their quality, reliability, and durability. “Plast” word in its name is totally misguiding.

Its business commenced with the manufacturing of Swaged MS Steel Tubular Poles in compliance with IS:2713 standards in a single pole manufacturing plant. Over the last three decades, it has developed a strong presence in this segment, supplying poles to various State Electricity Boards and private clienteles. As part of its backward integration strategy and expansion plan, the company installed two tube mills for manufacturing ERW steel pipes and tubes in various shapes and sizes as per standards such as IS:1161, IS:4270, IS:4923, IS:3589, IS:2713, and IS:9295 under the Bureau of Indian Standards Act, 2016.

As of the date of this Red Herring Prospectus (RHP), the company operates two manufacturing units located at (i) Plot No. B-4 & D-8, Industrial Area, Rania, District Kanpur Dehat, Uttar Pradesh (“Unit I”) and (ii) Khata No. 157 and 166, Gata No. 1354, Kisharwal, Akbarpur, Kanpur Dehat, Uttar Pradesh (“Unit II”). Unit I is primarily focused on the production of poles while, Unit II is equipped for the manufacturing of both ERW Steel Pipes and Swaged Steel Tubular Poles. Its products are rust-resistant and tailored to meet specific project and industry requirements. It has a wide distribution network extending across multiple states in India.

As on the date of this RHP, it has an installed capacity of 7,500 metric tonnes (MT) per month and 90,000 MT per annum for ERW steel pipes and tubes and 12,500 units per month and 1,50,000 units per annum for Swaged Steel Tubular Poles, based on a single shift basis. Its product portfolio currently comprises over 80 standard sizes in steel tubular poles, ranging from 410SP-1 to 410SP-80 as per IS:2713. The company manufactures round pipes from 1.5 inches to 8 inches in diameter and square hollow section pipes up to 100x100 mm, as well as other pipes and tubes in accordance with IS:3589, IS:4270, and IS:9295, in various diameters and thicknesses. It is in the process of expanding its products to include round pipes up to 10 inches and square pipes up to 200x200 mm. It supplies products in accordance with customer specifications, which may include galvanization, a process that enhances corrosion resistance and extends the service life of steel structures, particularly in outdoor and high-moisture environments. For galvanization our Company directly procures the required poles from a third-party vendor to supply it to customers. As of March 31, 2026, it had 35 employees on its payroll.

The company is coming out with its maiden book building route IPO of 3000000 equity shares of Rs. 10 each to mobilize Rs. 24.00 cr. RLL has announced the price band of Rs. 77 – Rs. 80 per share. The minimum application to be made is for 3200 shares and in multiples of 1600 shares thereon, thereafter. The issue opens for subscription on June 19, 2026 and will close on June 23, 2026. The shares will be listed on BSE SME. The IPO constitute 27.27% of the post-IPO paid-up capital of the company. From the net proceeds of the issue, the company will utilize Rs. 2.20 cr. for capex on new manufacturing facility for crash barriers and solar panel structures, Rs. 13.75 cr. for working capital, and the rest for general corporate purposes. The offer document is showing 27.72% dilution against the actual figure of 27.27% on page no. 3 of the offer document, as well as in IPO price band advertisement.

The IPO is solely lead managed by CapitalSquare Advisors Pvt. Ltd., and Bigshare Services Pvt. Ltd. is the registrar to the issue. CapitalSquare group’s CapitalSquare Financial Services Pvt. Ltd. is a market maker and as a syndicate member.

After issuing entire initial equity capital at par value, the company issued bonus shares in the ratio of 2 for 5 in March 2014, and 1 for 1 in September 2024. The average cost of acquisition of shares by the promoters is Rs. 3.78, Rs. 4.54, Rs. 4.76, and Rs. 5.00 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 8.00 cr. ill stand enhanced to Rs. 11.00 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 88.00 cr.

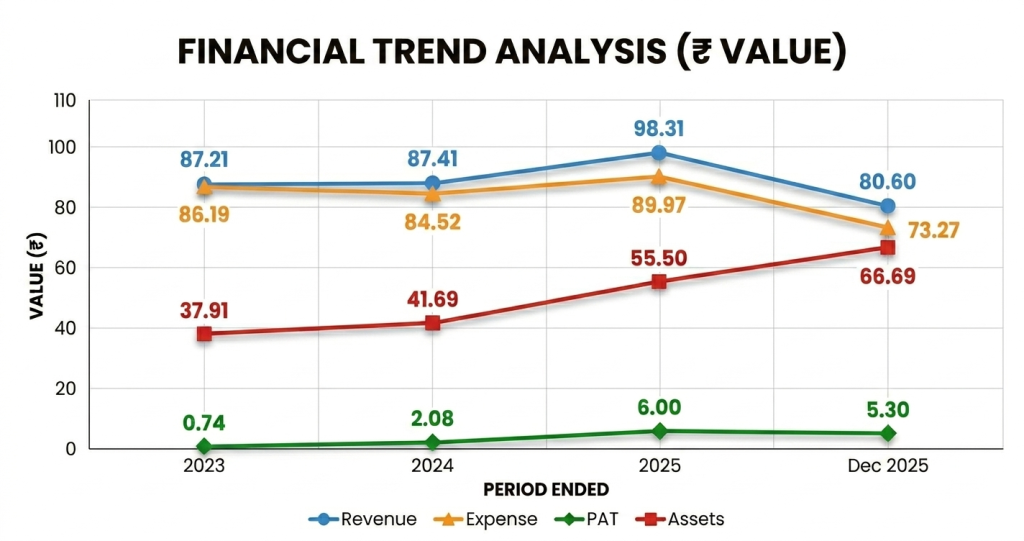

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 87.21 cr. / Rs. 0.74 cr. (FY23), Rs. 87.41 cr. / Rs. 2.08 cr. (FY24), Rs. 98.31 cr. / Rs. 6.00 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 5.30 cr. on a total income of Rs. 80.60 cr. The company reported static performance for FY23 and FY24, but marked jump in bottom lines for FY24. FY25 onwards it marked growth in its top and bottom lines. It operates in a highly competitive and fragmented segment, that raise concern over its sustainability in maintaining the margins going forward.

For the last three fiscals, the company has reported an average EPS of Rs. 4.77 and an average RoNW of 33.81%. The issue is priced at a P/BV of 3.07 based on its NAV of Rs. 26.06 per share as of December 31, 2025, but its post IPO NAV data is missing from the offer documents.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 12.46, and based on FY25 earnings, the P/E stands at 14.68. The issue appears aggressively priced based on its recent earnings.

The company has posted PAT Margins of 0.85% (FY23), 2.38% (FY24), 6.11% (FY25), 6.58% (9M-FY26), and ROCE margins of 26.88%, 38.67%, 62.25%, 42.65%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends since its incorporation. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown New Malayalam, P S Raj Steels, as its listed peers. They are trading at a P/E of 5.99 and 36.7 (as pf June 15, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears as an eyewash.

This is the 5th mandate from CapitalSquare Advisors in the last two fiscals (including the ongoing one). Out of the last 4 listings, all listed at discount to the offer price on listing date. The merchant banker has a poor track record.

APL is in the business of manufacturing of ERW steel pipes and tubes in sound and square hollow sections as well as swaged steel tubular poles. It offers various sizes and lengths of its products amidst its vast product portfolio. After static top lines for FY23 and FY24, the company posted growth in its top lines for the reported periods. However, boosted profits from FY24 onwards raise concern as it operates in a highly competitive and fragmented segments. Based on its recent financial performances, the issue appears aggressively priced. Merchant Banker has a poor track record. There is no harm in skipping this pricey and dicey IPO.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.