Twinkle Papers Ltd. (TPL) is manufacturer of Corrugated Boxes and polymer-based molded packaging products. It is engaged in this industry from the last 28 years. The company is located in Malerkotla (30 kms from Ludhiana) on Malerkotla Ludhiana Highway. Its journey began in 1999 with the installation of its first blow molding machine, which allowed it to start manufacturing poly jars and HDPE cans. Over time, TPL expanded its capabilities by introducing new technologies:

• In 2021, It installed an injection molding machine for manufacture plastic crates.

• In 2022, The company installed a rotational molding machine for making roto-molded pallets.

• In 2023, it further strengthened plastic product line by installing another injection molding machine to produce plastic pallets.

Today, TPL manufactures a wide range of packaging and material handling products, including:

1. Corrugated Boxes, 2. Plastic Pallets, 3. Crates, 4. HDPE Cans, Poly Jars, Jerry Cans, and Drums, 5. Polythene Sheets and Poly Bags, 6. Plastic Chairs. Its plastic products are made using advanced technologies like blow molding, injection molding, and rotational molding. These are mainly used in industries such as food, dairy, construction chemicals, pharmaceuticals, textiles, and more. The company sells all products under the brand name “Twinkle”, catering to a diverse range of industries. Its inhouse R&D team works closely with clients to design custom polymer solutions that address their specific packaging challenges. Its Manufacturing facilities also complies with ISO 9000: 2015 systems.

Its capacity utilization has gradually increased from 67.04% for FY23 to 79.40% for 9M-FY26. As of April 30, 2026, it had 147 employees on its payroll.

The company is coming out with its maiden book building route IPO of 3988000 equity shares of Rs. 10 each to mobilize Rs. 27.52 cr. The company has announced a price band of Rs. 64 – Rs. 69 per share. The minimum application to be made is for 4000 shares and in multiples of 2000 shares thereon, thereafter. The issue opens for subscription on June 29, 2026 and will close on July 01, 2026. The shares will be listed on BSE SME. The IPO constitute 26.32% of the post-IPO paid-up capital of the company. From the net proceeds of the issue, the company will utilize Rs. 6.50 cr. for capex on purchase of new machineries, Rs. 7.00 cr. for Repayment of portion of loans, Rs. 8.00 cr. for working capital, and the rest for general corporate purposes.

The IPO is solely lead managed by Novus Capital Advisors Pvt. Ltd., and Alankit Assignments Ltd. is the registrar to the issue. Nirman Share Brokers Pvt. Ltd. is a market maker.

After issuing entire equity capital at par value, the company issued further equity shares in the price range of Rs. 35 – Rs. 60 per share between March 2008 and March 2025. It has also issue bonus shares in the ratio of 10 for 1 in September 2024. The offer document is missing data on average cost of acquisition of shares by the promoters.

Post-IPO, company’s current paid-up equity capital of Rs. 11.16 cr. will stand enhanced to Rs. 15.15 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 104.54 cr.

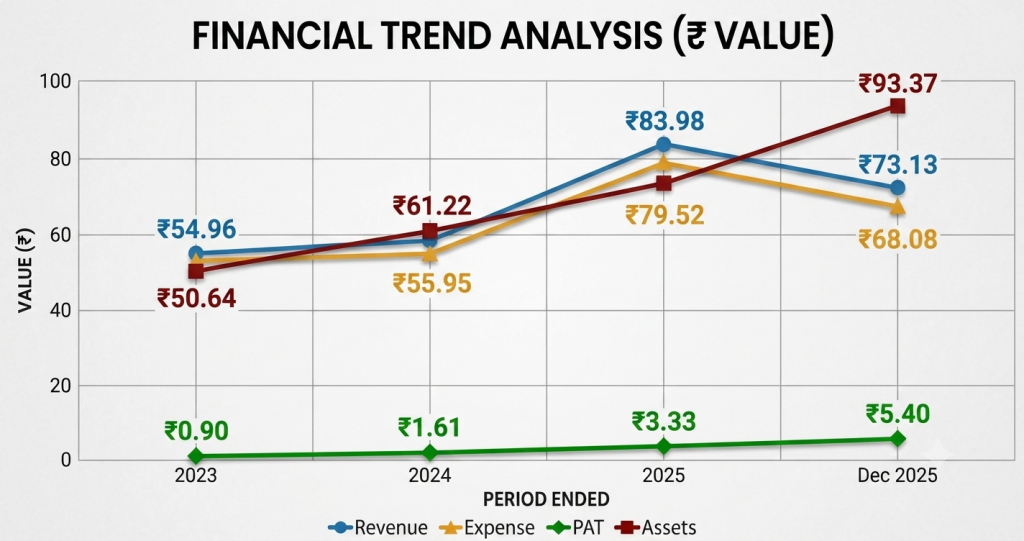

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 54.96 cr. / Rs. 0.90 cr. (FY23), Rs. 58.75 cr. / Rs. 1.61 cr. (FY24), Rs. 83.98 cr. / Rs. 3.33 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 5.40 cr. on a total income of Rs. 73.13 cr. The company posted growth in its top and bottom lines for the reported periods, but its profit margins galloped from FY24 onwards following its product shift from low margins to high margins plastic products, informed the management.

For the last three fiscals, the company has reported an average EPS of Rs. 2.34 and an average RoNW of 15.26%. The issue is priced at a P/BV of 3.09 based on its NAV of Rs. 22.34 per share as of December 31, 2025, but its post IPO NAV data is missing from the offer documents.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 14.53, and based on FY25 earnings, the P/E stands at 31.51. The issue appears fully priced based on its recent earnings.

The company has posted PAT Margins of 1.65% (FY23), 2.76% (FY24), 4.25% (FY25), 7.49% (9M-FY26), and ROCE margins of 20.48%, 29.96%, 22.83%, 18.82%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown TPL Plastech, Prima Plastic, Pyramid Technoplast, as its listed peers. They are trading at a P/E of 19.3, 6.61, and 22 (as of June 25, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears as an eyewash.

This is the 14th mandate from Novus Capital Advisors in the last three fiscals (including the ongoing one). Out of the last 13 listings, 4 closed at discount to offer price on the date of listings.

TPL is engaged in manufacturing and marketing of corrugated boxes, moulded packaging products, plastic furniture, pallets, crates etc. The company marked growth in its top and bottom lines for the reported periods. It is operating in a highly competitive and fragmented segment. Based on its recent financial data, the issue appears fully priced. Only well-informed/cash surplus investors may park moderate funds for long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.