Teja Engineering IPO Review (NSE SME)

Teja Engineering Industries Ltd. (TEIL) provides services across Operation & Maintenance (O&M) including Annual Maintenance Contracts (AMC), Erection & Commissioning (E&C) including project works, installation of stainless-steel tubing, Overhauling, Decommissioning & Recommissioning. The company also undertakes instrument calibration, non-destructive thickness testing of pressure vessels, and testing and servicing of safety relief valves (SRVs). TEIL operates in the Oil & Gas, Power, and Energy sectors, supporting OEMs, CNG compressor packagers, and public sector undertakings involved in gas distribution and energy infrastructure.

With a network extending across India, the company provides technical knowledgeable manpower and execution support for CNG stations, gas compression plants, and natural gas distribution terminals. The company’s role is to ensure smooth and efficient operation of energy infrastructure, though it does not manufacture equipment itself.

Its workforce of 1994 is deployed across client sites to deliver Operations & Maintenance, Erection & Commissioning, installation, overhauling, and recommissioning services. TEIL’s main area of service is Operations & Maintenance (O&M). As on the date of this Prospectus, it has expanded services to 15 states: Gujarat, Maharashtra, Telangana, Andhra Pradesh, Tamil Nadu, Kerala, Karnataka, Goa (UT), Madhya Pradesh, Rajasthan, Odisha, West Bengal, Bihar, Tripura and Jharkhand

Its work includes Erection, Installation, Testing, Commissioning, Operation and maintaining, natural gas compression stations to ensure smooth and reliable operations. This allows it to handle projects of different scales and requirements effectively. The company has completed over 300+ CNG compressor station projects and manages O&M services for more than 550 units pan India. Its expertise spans the entire lifecycle of gas and energy projects from commissioning to operation and maintenance enabling it to effectively support customers in the CGD sector.

The Company, together with the track record of the erstwhile proprietorship firm M/s Teja Engineering Services (TES), has completed 397 E&C sites, as certified by Chartered Engineer Kishan C. Korat (Registration No. AM1958561) on September 28, 2025. As of November 30, 2025, the Company is managing 728 active O&M sites. As of May 31, 2026, it had 2927 employees on its payroll.

Issue Details / Capital History

The company is coming out with its maiden IPO of 1698000 equity shares of Rs. 10 each at a fixed price of Rs. 220 per share to mobilize Rs. 37.36 cr. at the upper cap. The minimum application to be made is for 2400 shares and in multiples of 1200 shares thereon, thereafter. The IPO opens for subscription on June 30, 2026, and will close on July 02, 2026. The IPO constitute 26.46% of the post-IPO paid-up capital of the company. The shares will be listed on NSE SME Emerge. The company is spending Rs. 4.59 cr. for this IPO process, and from the net proceeds of the IPO, it will utilize Rs. 9.26 cr. for working capital, Rs. 18.01 cr. for capex on purchase of equipment/machineries, and Rs. 5.50 cr. for general corporate purposes.

The IPO is solely lead managed by Interactive Financial Services Ltd., and KFin Technologies Ltd., is the registrar to the issue. B N Rathi Securities Ltd., is the market maker.

The company has issued/converted initial equity capital at par value. It has issued further equity shares at a fixed price of Rs. 150 per share in December 2024.The average cost of acquisition of shares by the promoters is Rs. 10 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 4.72 cr. will stand enhanced to Rs. 6.42 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 141.18 cr.

IPO Lead Managers & Registrar

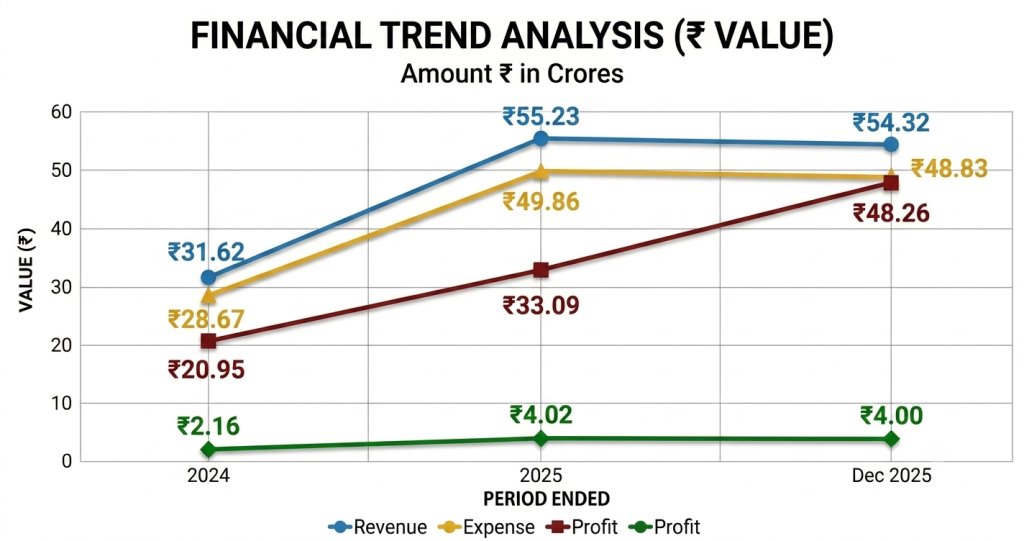

On the financial performance front, for the last three fiscals, the company has reported a total income/net profit of Rs. 24.58 cr. / Rs. 1.27 cr. (FY23-as proprietorship entity), Rs. 40.02 cr. / Rs. 2.53 cr. (FY24-as public limited co.), Rs. 55.23 cr. / Rs. 4.02 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 4.00 cr. on a total income of Rs.54.32 cr. The company marked growth in its top and bottom lines for the reported periods.

For the reported period, the company has reported an average EPS of Rs. 7.91, and an average RoNW of 32.29%. The issue is priced at a P/BV of 6.24 based on its NAV of Rs. 35.24 per share as of March 31, 2026, and at a P/BV of 2.62 based on its post-IPO NAV of Rs. 84.13 per share, at the upper cap.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 26.44, and based on FY25 earnings, the P/E stands at 35.14. The issue appears exorbitantly priced, based on its recent earnings.

For the reported periods, the company has posted PAT margins of 4.56% (FY24), 7.69% (FY25), 9.84% (FY26), and RoCE margins of 15.25%, 17.58%, 18.47%, respectively, for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividend for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has shown Lakshya Powertech, as its listed peer. It is currently trading at a P/E of 11.1 (as of June 22., 2026. However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

Merchant Banker's Track Record

This is the 32nd mandate from Interactive Financial in the last five fiscals (including the ongoing one). Out of the last 12 listings, 7 opened at discount, 1 at par, and the rest listed with a premium ranging from 1.10% to 6.53% on the listing date. The merchant banker has a poor track record.

Conclusion

TEIL is engaged in providing services across O&M, AMC, E&C, projects for gas. The company posted growth in its top and bottom lines for the reported periods. The company operates in a highly competitive and fragmented segment. Sustainability of its profit margins remains major concern. Small paid-up equity capital post-IPO indicates longer gestation for migration. The merchant banker has a poor track record. Investors can avoid this pricey and dicey IPO.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.