Knack Packaging IPO Review

Knack Packaging Ltd. (KPL) is one of the leading, integrated, innovation-oriented, export led and sustainable oriented packaging solutions provider, offering a diverse range of packaging solutions, including Printed and Laminated Woven Polypropylene (“PLWPP”) bags and PLWPP Pinch Bottom bags that are customized, high-strength packaging solutions for a wide range of sectors, including food products and pet foods (Source: Technopak Report). Its solutions enhance brand visibility on packaging, reduce the risk of counterfeiting, and improve operational performance. It holds approximately 10.1% of market share in the Indian market for flexible bulk PLWPP bags, including PLWPP pinch bottom bags in Fiscal 2025 (Source: Technopak Report). KPL is also one of the early movers in the manufacturing of BOPP/ PLWPP bags, and the first company in India (and Asia) to provide laser cut and easy-open feature integrated into their PLWPP pinch bottom bags (Source: Technopak Report).

With a legacy of over two decades, it offers a wide array of bulk packaging solution which has been developed over the decades through technological enhancements and industry experience. The company also provides add-on solutions such as circular & back seam construction, half, full & register window, zig-zag cut, heatcut & bladecut etc., providing customers with enhanced and customized packaging options. Its diverse range of packaging solutions along with customised add-ons, makes it a one stop solution for customers.

The company has been serving top brands under a B2B2C model, including household Indian names such as Baba Agro Food Limited, Drools Pet Food Private Limited, Ebro India Private Limited, Laxmi Protein Products Pvt. Limited, Mosaic India Private Limited, KRBL Limited, Shriram Woven Sacks and DCM Shriram Limited, as well as international brands across 71 countries like Cristo S.A., Sacos y Empaques Internacionales S.A. de C.V., Cargill and Repi Soap and Detergent PLC. These brands use KPL’s 5kg to 50kg packaging solutions, to offer their products which are typically in powder or granule form, to their respective customers. The key industries which it serves include grains and pulses – rice, dal, lentils, etc., flour & spices, sugar, salts, fruits & nuts, animal & pet foods, agriculture, seeds, charcoal, detergents powders & granules, fertilizers, chemicals, cement, tile adhesives, building materials, mineral bags etc. (Source: Technopak Report)

While its product portfolio includes a variety of flexible packaging solutions, its PLWPP Bags with laser cut and easy open features stand out due to its several advantages over conventional woven bags. The company has also been officially recognized as a Two Star Export House by the Government of India. Its customer retention ratio improved from 67.27% (FY24) to 88.32% (FY26). Its export revenue accounted for 56.30% for FY26. According to the management, they have major thrust for exports and such trends will continue going forward.

The Company has established Sayem Knack, a joint venture with SACOS Y Empaques Internacionales to develop a new manufacturing facility that supports its expansion into Latin America and the United States. KPL’s Joint Venture recently commenced its commercial operations on April 6, 2026, enhancing its ability to serve regional and multinational clients more effectively. In addition to the geographic advantages, its Joint Venture enables technological collaboration, shared research & development efforts, and the co-development of new-aged packaging solutions. As of March 31, 2026, it had 1834 employees (including 659 contract labour).

Issue Details / Capital History

The company is coming out with its maiden book building route combo IPO of Rs. 380.00 cr. (approx. 22352941 equity shares of Rs. 10 each at the upper cap), and an offer for sale (OFS) of 3500000 equity shares (worth Rs. 59.50 cr. at the upper cap). The company has announced a price band of Rs. 161 – Rs. 170 per equity shares of Rs. 10 each. The overall size of the IPO shall be 25852941 equity shares at the upper cap amounting to Rs. 439.50 cr. The issue opens for subscription on July 01, 2026, and will close on July 03, 2026. The minimum application to be made is for 88 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 21.13% of the post-IPO paid-up equity capital. From the net proceeds of the fresh equity issue, the company will utilize Rs. 320.00 cr. for capex on setting up of new manufacturing facility at Mehsana-Gujarat, and the rest for general corporate purposes.

The company has reserved equity shares worth Rs. 2 cr. for its eligible employees and offering them a discount of Rs. 16 per share. From the rest, it has allocated not more than 50% for QIBs, not less than 15% for HNIs, and not less than 35% for Retail investors.

The joint Book Running Lead Managers (BRLMs) to this issue are Systematix Corporate Services Ltd., IDBI Capital Markets & Securities Ltd., Pantomath Capital Advisors Pvt. Ltd., and MUFG Intime India Pvt. Ltd. is the registrar to the issue. Systematix Share & Stocks (India) Ltd., Asit C Mehta Investment Interrmediates Ltd., are the syndicate members.

The company has issued initial equity shares at par value, and has also issued bonus shares in the ratio of 19 for 1 in May 2025. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. 2.86, Rs. 5.00, Rs. 7.50, and per share.

Post-IPO, its current paid-up equity capital of Rs. 100.00 cr. will stand enhanced to Rs. 122.35 cr. Based on the upper cap of the price band, the company is looking for a market cap of Rs. 2080.00 cr.

IPO Lead Managers & Registrar

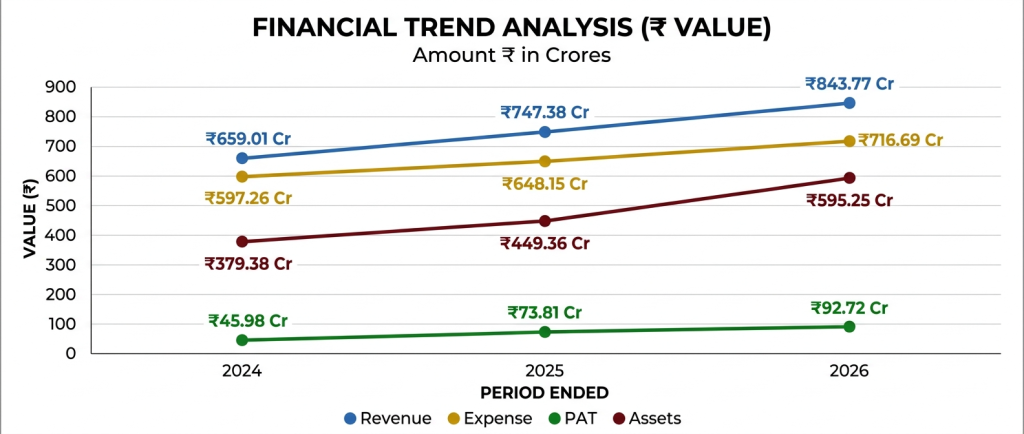

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted a total income/net profit, of Rs. 659.01 cr. / Rs. 45.98 cr. (FY24), Rs. 747.38 cr. / Rs. 73.81 cr. (FY25), and Rs. 843.77 cr. / Rs. 92.72 cr. (FY26). The company posted steady growth in its top and bottom lines for the reported periods.

For the last three fiscals, the company has posted an average EPS of Rs. 7.86 and an average RoNW of 38.08 %. The issue is priced at a P/BV of 5.52 based on its NAV of Rs. 30.82 as of December 31, 2025, and at a P/BV of 3.02 based on its post-IPO NAV of Rs. 56.24 per share at the upper cap.

If we attribute FY26 earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 22.43. Based on FY25 earnings, the P/E stands at 28.19. The issue appears fully priced.

For the reported periods, while the company has posted PAT margins of 6.98 % (FY24), 9.88% (FY25), 10.99% (FY26), and RoCE margins of 45.42%, 50.36%, 46.71%, respectively for the referred periods.

All amounts in Indian Rupees crores

The company not paid any dividends for the reported periods of the offer document. It has already adopted a dividend policy in August 2025, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has shown Time Techno Plast, TCPL Packaging, Mold-Tek Packaging, as its listed peers. They are currently trading at a P/E of 19.2, 25.6, and 31.7 (as of June 25, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

Merchant Banker's Track Record

The three BRLMs associated with this issue have handled 18 issues in the last 3 fiscals (including the ongoing one), out of which 7 issues closed below the offer price on listing date.

Conclusion

KPL is one of the leading, integrated, innovation-oriented, export led and sustainable oriented packaging solution provider globally. Its JV at Latin America-US has gone on stream in April 2026, will contribute in its export earnings. The company marked steady growth in its top and bottom lines for the reported periods. Based on its recent financial data, the issue appears fully priced. Considering bright prospects for packaging industry ahead, investors can park funds for medium to long term rewards.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.