Jivial Industries IPO Review (BSE SME)

Jivial Industries Ltd. (JIL) is manufacturing finished aluminium railings and fixtures from unfinished extruded aluminium railings and unfinished aluminium castings, as per the specifications and requirements of customers. The company engineers the aluminium railings and fixtures at its factory to hold glass for partitions, balconies, viewing windows, façade of buildings etc. It manufactures majorly two types of railings; (i) Continuous Profiles, used for holding the glass at the bottom and; (ii) Handrails for holding the glass at the top along with design for hand support. Further, the company manufactures several aluminium fixtures used in supporting the railings to hold glass, such as, spigot, conceal, bend, bracket, jointer, lock and endcap.

JIL has been successful in obtaining 3 patents for its unique product design of Spigots from, The Patent Office, Government of India. The aluminium railings and fixtures are manufactured by cutting, drilling, anodizing, buff polishing and powder coating as per the requirements of customers. Its customers are mainly small and medium level construction companies, architects, interior designers, glass providers and fabricators. The company caters to customers all over India but majority revenues are generated from Gujarat, Maharashtra and Chhattisgarh which total 72.87%, 67.82% and 62.55% of its total revenues in FY 2025, FY 2024 and FY 2023 respectively. It is operating in a highly competitive and fragmented segment. As of May 31, 2026, it had 19 employees on its payroll.

Issue Details / Capital History

The company is coming out with its maiden book building route combo IPO of 1632000 equity shares of Rs. 10 each at a fixed price of Rs. 196 per share to mobilize Rs. 31.99 cr. The IPO consists of 1359600 fresh equity shares (worth Rs. 26.65 cr.), and an Offer for Sale (OFS) of 272400 equity shares (worth Rs. 5.34 cr.) The minimum application to be made is for 1200 shares and in multiples of 600 shares thereon, thereafter. The issue opens for subscription on June 23, 2026 and will close on June 25, 2026. The shares will be listed on BSE SME. The IPO constitute 34.95% of the post-IPO paid-up capital of the company. The company is spending Rs. 4.25 cr. for fresh issue process, and from the net proceeds of the issue, the company will utilize Rs. 14.40 cr. for capex on purchase of new machineries, Rs. 4.00 cr. for capex on renovation of existing facility, and Rs. 3.99 for general corporate purposes.

The IPO is solely lead managed by Corporate Makers Capital Ltd., and Bigshare Services Pvt. Ltd. is the registrar to the issue. Sunflower Broking Pvt. Ltd. is a market maker. The IPO is underwritten to the tune of 15% by Corporate Makers and 85% by Sunflower Broking.

After issuing entire equity capital at par value, the company issued bonus shares in the ratio of 150 for 1 in September 2023. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. 5.79, and Rs. 6.22 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 3.31 cr. will stand enhanced to Rs. 4.67 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 91.52 cr.

IPO Lead Managers & Registrar

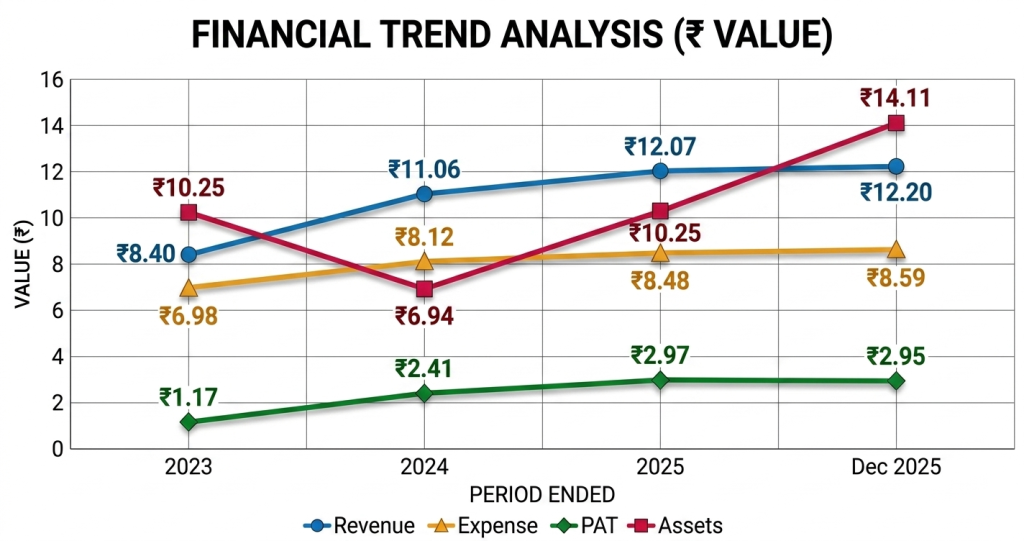

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 8.40 cr. / Rs. 1.17 cr. (FY23), Rs. 11.06 cr. / Rs. 2.41 cr. (FY24), Rs. 12.07 cr. / Rs. 2.97 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 2.95 cr. on a total income of Rs. 12.20 cr. The company growth in its top and bottom lines for the reported periods, but its profit margins are raising eyebrows and concern over its sustainability going forward as it is operating in a highly competitive and fragmented segment.

For the last three fiscals, the company has reported an average EPS of Rs. 9.17 and an average RoNW of 63.14%. The issue is priced at a P/BV of 5.56 based on its NAV of Rs. 35.24 per share as of December 31, 2025, and at a P/BV of 2.39 based on its post IPO NAV of Rs. 82.05 per share.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 23.28, and based on FY25 earnings, the P/E stands at 30.82. The issue appears aggressively priced based on its recent earnings.

The company has posted PAT Margins of 13.89% (FY23), 21.82% (FY24), 24.75% (FY25), 24.33% (9M-FY26), and ROCE margins of 136.49%, 75.36%, 46.79%, 33.14%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has shown ANB Metal Cast, Euro Panel Products, Sudal Ind. as its listed peers. They are trading at a P/E of 26.6, 16.1, and NA (as pf June 19, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears as an eyewash.

Merchant Banker's Track Record

This is the 10th mandate from Corporate Makers in the last three fiscals (including the ongoing one). Out of the last 9 listings, 5 opened at discount, 3 at par, and 1 at a premium of 53.38%. The merchant banker has a poor track record.

Conclusion

JIL is engaged in the manufacturing and marketing of finished aluminium railings and fixtures from unfinished extruded aluminium railings and castings. It posted growth in its top and bottom lines for the reported periods. Majority of its revenue comes from Gujarat, Maharashtra and Chhatisgarh. The surprising margins reported by it may not sustain as it is operating in a highly competitive and fragmented segment. Based on its recent financial data, the issue appears aggressively priced. Tiny equity base post-IPO indicates longer gestation period for migration. There is no harm in skipping this pricey and dicey IPO.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.