Hexagon Nutrition Ltd. (HNL) is a differentiated and research-oriented pure play nutrition Company. The company is holistic nutrition player that offers products across a whole range starting with micronutrient premixes, right up to therapeutic and clinical products (Source: CARE Report). It is also one of the largest premix players in India, offering customized vitamin and mineral premixes to leading Indian and multinational FMCG companies. It is also one of the largest licensed suppliers of Micronutrient Powders (MNPs) under UN programmes, supporting global food fortification and public health initiatives (Source: CARE Report). HNL’s product portfolio addresses a broad spectrum of nutritional aspects such as fortification of foods, therapeutic nutrition, clinical nutrition and alleviation of malnutrition.

It is a fully integrated company engaged across the entire value chain, right from research and product development to manufacturing and marketing, with a focus on quality. The Company began its journey in the year 1993 as a micronutrient formulations player and has steadily moved up the value chain to develop its brands such as “PENTASURE”, “OBESIGO” and “PEDIAGOLD” in the health, wellness, and clinical nutrition space. In Fiscal 2024, the Company further expanded its portfolio with the launch of a new brand, “NUTRONE”, strengthening its position in the segment. Its presence spans across India, and products have been exported to over 75 countries during the nine month period ended December 31, 2025 and Fiscals 2023, 2024 and 2025.

It operates three (3) manufacturing facilities in India, located in Nasik (Maharashtra), Chennai (Tamil Nadu) and Thoothukudi (Tamil Nadu), along with one (1) international manufacturing facility in Tashkent, Uzbekistan. Two of its Indian manufacturing facilities is situated in SEZ zones in Chennai (Tamil Nadu) and Thoothukudi (Tamil Nadu) and offers strategic advantages such as proximity to major ports and access to duty-free imports.

The Company has a PAN-India omnichannel distribution network, supported by its presence across retail pharmacies, hospital networks, e-commerce platforms, and own websites including www.pentasurenutrition.com, www.obesigo.com, www.pediagold.com and www.nutrone.fit. During the nine month period ended December 31, 2025, its sales force of over 160 members actively engaged with approximately over 20,000 healthcare professionals across India to recommend its branded nutrition products. Further, for domestic distribution, it relies on growing network of over 350 non-exclusive distributors strategically located across India including 8 distributors who have presence in multiple states. This network allows it to respond effectively to market demands, adapt to evolving consumer preferences, and navigate competitive pressures in both metro and non-metro

markets. The company follows B2B2C model operations

Internationally, its distribution network extends across non-exclusive 20 regional distributors covering North and South America, Southeast Asia, Africa, and the Middle East. As of March 31, 2026, it had 527 employees on its payroll, and addition 513 contract manpower engaged through contractors in various departments.

According to the management, considering their capabilities with in-house R & D, Research centers, they are capable of meeting the customers requirements with rising demand. The company is poised for improved performance going forward looking at the influx of orders.

The company is coming out with its maiden book building route secondary IPO of 30859704 equity shares of Re. 1 each to mobilize Rs. 138.86 cr. at the upper cap. The IPO is entirely as an Ofer for Sale (OFS); hence no funds are going to the company. The company has announced a price band of Rs. 42 – Rs. 45 per equity shares of Re. 1 each. The issue opens for subscription on June 05, 2026, and will close on June 09, 2026. The minimum application to be made is for 333 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 25.11% of the post-IPO paid-up equity capital. The OFS is being made to unlock its value, provide exit to its stakeholders and listing benefits.

The joint Book Running Lead Managers (BRLMs) to this issue are Cumulative Capital Pvt. Ltd., and Catalyst Capital Partners Pvt. Ltd., while KFin Technologies Ltd., is the registrar to the issue. Cumulative Capital Pvt. Ltd., Catalyst Capital Partners Pvt. Ltd. and Nikunj Stock Brokers Ltd. are syndicate members.

After issuing/converting initial equity shares at par, the company has issued/converted further equity shares in the price range of Rs. 2.61 – Rs. 20.48 per share (on the basis of Re. 1 FV) between July 2016 – April 2026. It has also issued bonus shares in the ratio of 5 for 1 in September 2008, and 2 for 1 in November 2014. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. 0.43, Rs. 0.48, Rs. 0.51, Rs. 0.65, Rs. 0.92, and Rs. 1.27 per share.

Post-IPO, its current paid-up equity capital of Rs. 12.29 cr. will remain same as this is a pure secondary issue. Based on the upper band of price, the company is looking for a market cap of Rs. 553.13 cr.

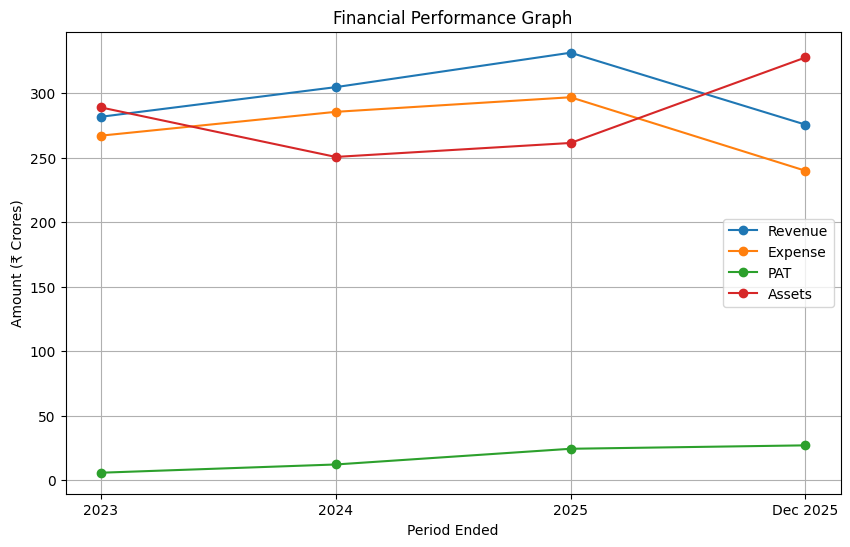

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted a total income/net profit, of Rs. 281.65 cr. / Rs. 5.82 cr. (FY23), Rs. 304.62 cr. / Rs. 12.21 cr. (FY24), and Rs. 331.29 cr. / Rs. 24.38 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 27.03 cr. on a total income of Rs. 275.57 cr.

For the last three fiscals, the company has posted an average EPS of Rs. 1.29 and an average RoNW of 9.13 %. The issue is priced at a P/BV of 2.48 based on its NAV of Rs. 18.15 as of December 31, 2025, as well as on post IPO basis.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 15.36. Based on FY25 earnings, the P/E stands at 22.73. The issue appears fully priced based on its recent financial data.

For the reported periods, while the company has posted PAT margins of 2.07% (FY23), 4.01% (FY24), 7.36% (FY25), 9.81% (9M-FY26), and RoCE margins of margins 5.94%, 11.12%, 17.06%, 14.82%, respectively for the reported periods.

All amounts in Indian Rupees crores

The company paid a dividend of 15% for FY23, but there after it skipped. It has already adopted a dividend policy in November 2021, based on its financial performance and future prospects.

As per the offer document, the company has shown Zydus Wellness, Nestle India, as its listed peers. They are currently trading at a P/E of 69.5, and 79.4 (as of May 29, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

The two BRLMs associated with this issue, while Cumulative Capital has handled 7 issues in the last 3 fiscals, out of which no issues closed below the offer price on listing date. This is the first mandate from Catalyst Capital Partner. Both the BRLM are having first mainboard mandate, and have no track records, while Cumulative Capital had 7 SME IPO mandates.

HNL is a pure play nutrition company having differentiated and research-oriented products play. It posted steady growth in its top and bottom lines for the reported periods. It is a most preferred partner/supplier for nutritional products with a rising market share. Based on its recent financial data, the issue appears fully priced. Well-informed investors may park funds for medium to long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.