Avience Biomedicals IPO Review (NSE SME)

Avience Biomedicals Ltd. (ABL) is a medical consumable company dedicated to manufacturing of Vitro-Diagnostic (IVD) products and medical devices in Noida, Uttar Pradesh, India. In vitro diagnostics (IVDs) are tests that can detect disease, conditions and infections. In vitro simply means ‘in glass’, meaning these tests are typically conducted in test tubes and similar equipment, as opposed to in vivo tests, which are conducted in the body itself. In vitro tests can be done in laboratories, health care facilities or even in the home.

The tests themselves can be performed on a variety of instruments ranging from small, handheld tests to complex laboratory instruments. It has emerged as innovative diagnostics solutions provider. Recognized as a Startup and a Small-scale Industry under MSME, Company is committed to empowering healthcare professionals with advance technology.

ABL commenced its journey by producing essential diagnostic kits like Viral Transport Media (VTM), Covid, Human Immunodeficiency Viruses (HIV), HBs AG, Malaria, Dengue and others aimed at aiding medical institutions with affordable and good-quality solutions. The company has expanded its product range from IVD rapid test kits to include a comprehensive line of medical devices such as Serology products, Biochemistry Analyzer and Biochemistry Reagents, showcasing a dedication to addressing various healthcare needs. Being majorly into B2B and B2C market, its products cater to Pathology Labs, Microbiology Labs, Hospitals, and Research Centers nationwide as well as overseas. In addition to manufacturing, the Company also act as distributors and traders of medical equipment. As of the date of this offer document, it has 75 employees on its payroll, including the contract workers.

Issue Details / Capital History

The company is coming out with its maiden book building route IPO of 1453800 equity shares of Rs. 10 each to mobilize Rs. 30.24 cr. at the upper cap. The company has announced a price band of Rs. 196 - Rs. 208 per share. The minimum application to be made is for 1200 shares and in multiples of 600 shares thereon, thereafter. The IPO opens for subscription on June 18, 2026, and will close on June 22, 2026. The IPO constitute 26.50% of the post-IPO paid-up capital of the company. The shares will be listed on NSE SME Emerge. From the net proceeds of the IPO, it will utilize Rs. 15.95 cr. for capex on setting up of new manufacturing facility at YEIDA – UP., Rs. 8.25 cr. for working capital, and the rest for general corporate purposes.

The IPO is solely lead managed by Fintellectual Corporate Advisors Pvt. Ltd., and Skyline Financial Services Pvt. Ltd., is the registrar to the issue. Asnani Stock Brokers Pvt. Ltd., is the market maker. The issue is underwritten to the tune of 20.02% by Fintellectual Corporate and up to 79.98% by Seren Capital Pvt. Ltd.

After issuing initial equity capital at par value, the company issued further equity shares at Rs/ 125 per share in July 2024, and August 2024. It has also issued bonus shares in the ratio of 1 for 3.379 in March 2023. The average cost of acquisition of shares by the promoters is Rs. NIL, Rs. 7.73, Rs. 12.28, and Rs. 24.17 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 4.03 cr. will stand enhanced to Rs. 5.48 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 114.09 cr.

IPO Lead Managers & Registrar

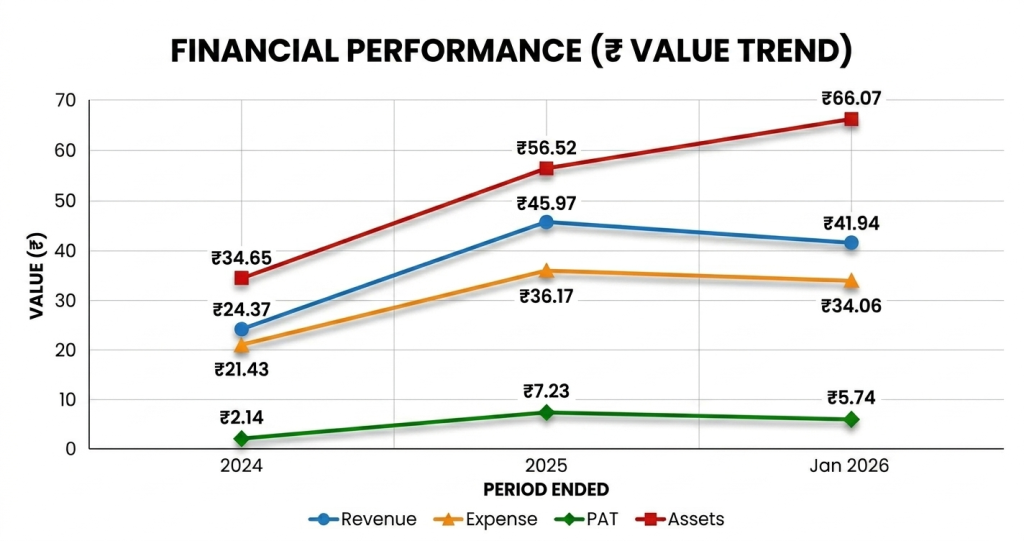

On the financial performance front, for the last two fiscals, the company has (on a consolidated basis) posted total revenue/ net profit, of Rs. 24.37 cr. / Rs. 2.14 cr. (FY24), Rs. 45.97 cr. / Rs. 7.23 cr. (FY25). For 10M of FY26 ended on January 31, 2026, it earned a net profit of Rs. 5.74 cr. on a total revenue of Rs. 41.94 cr. The boosted profits from FY25 onwards raise eyebrows and concern over its sustainability as it is operating in a highly competitive and fragmented segment.

On a standalone basis, for the last three fiscals, the company reported a total revenue/net profit of Rs. 10.93 cr. / Rs. 0.71 cr. (FY23), Rs. 16.64 cr. / Rs. 1.98 cr. (FY24), Rs. 29.54 cr. / Rs. 5.13 cr. (FY25). For 10M of FY26 ended on January 31, 2026, it earned a net profit of Rs.4.18 cr. on a total revenue of Rs.28.85 cr. Thus, the company marked spectacular performance on a consolidated basis.

For the reported period, the company has reported an average EPS of Rs. 14.88 (consolidated basis), and an average RoNW of 44.75%. The issue is priced at a P/BV of 2.94 based on its NAV of Rs. 70.74 per share as of March 31, 2026, and at a P/BV of 1.94 based on its post-IPO NAV of Rs. 107.12 per share (at the upper cap).

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 16.56, and based on FY25 earnings, the P/E stands at 15.78. The issue appears fully priced, based on its recent bumper earnings.

For the reported periods, the company has posted PAT margins of 8.83% (FY24), 15.86% (FY25), 13.68% (10M-FY26), and RoCE margins of 17.97%, 24.88%, 16.99%, respectively, for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has no listed pers to compare with.

Merchant Banker's Track Record

This is the 5th mandate from Fintellectual Corporate Advisors in the last three fiscals (including the ongoing one). Out of the last 4 listings, 1 opened at discount, and the rest listed with a premium ranging from 4.17% to 90.00% on the listing date.

Conclusion

ABL is engaged as a medical consumable product manufacturer as well as a trader. It operates in B2B as well as B2C segments providing advance technology products. ABL marked steady growth in its top and bottom lines for the reported periods. Based on its recent financial data, the issue appears fully priced. Tiny paid-up equity capital post-IPO indicates longer gestation period for migration. Well-informed/cash surplus investors may park moderate funds for long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.