Millworks Technologies Ltd. (MTL) is a precision engineering company engaged in the manufacture of machined components, sheet metal parts, and integrated assemblies used in mission-critical applications across the railways, aerospace, defence, and semiconductor sectors. Its operations are undertaken under Build-to-Print (BTP) and Build-to-Spec (BTS) engagement models and include both full-scope manufacturing as well as job-work arrangements. Under the BTP (Build-to-Print) model, manufacturing is carried out in accordance with customer-provided drawings and technical specifications, while under the BTS (Build-to-Spec) model, customers specify functional and performance requirements and the Company undertakes manufacturing to meet such specifications. This dual model enables it to support a diverse array of customer needs from strict adherence to design intent to more collaborative, performance-driven development.

Incorporated in 2021, the Company has developed into a multi-sector engineering enterprise with manufacturing capabilities spanning precision machining, sheet metal fabrication, sub-assembly, and related processes. It primarily supplies to Original Equipment Manufacturers (OEMs) Its quality systems and process controls are designed to meet rigorous industry standards, ensuring that every component and assembly it supplies performs reliably in the most demanding environments.

MTL’s manufacturing operations are supported by structured quality management systems. The Company has implemented and maintains a Quality Management System certified under AS9100D and ISO 9001:2015 on a multi-site basis. Unit I and Unit II are certified for the manufacture and supply of precision machined components for aerospace, defence and other industrial applications. Unit III is certified for the manufacture, supply and assembly of precision machined components and sheet metal parts for aerospace, defence, rail and other industrial applications. Unit IV is certified for the manufacture and supply of precision machined components for aerospace, defence and other industrial applications, and manufacture and supply of springs and wire forms for engineering applications. Company’s quality assurance infrastructure includes coordinate measuring machines (CMMs), video measuring systems, hardness testers, and calibrated measuring instruments. Quality records, inspection reports, and material traceability documentation are maintained in accordance with customer and applicable regulatory requirements.

For the fiscal 2026, its revenue from operations was Rs. 148.77 cr., of which 27.47% was derived from exports to customers located in 9 countries, including Canada, United States of America, Israel, Germany, France, Macedonia, Italy, United Kingdom, and Czech Republic. Its export operations primarily cater to customers in the aerospace and semiconductor machinery segments. Its top 10 customers have contributed on an average 91% of its revenues for the last three fiscals. As of April 30, 2026, it had 161 employees on its payroll, and additional 20 contract workers. As of June 05, 2026, it had an order book worth Rs. 67.14 cr.

The company is coming out with its maiden book building route IPO of 4844000 equity shares of Rs. 10 each to mobilize Rs. 160.34 cr. at the upper cap. The company has announced the price band of Rs. 315 – Rs. 331 per share. The minimum application to be made is for 800 shares and in multiples of 400 shares thereon, thereafter. The issue opens for subscription on July 14, 2026 and will close on July 16, 2026. The shares will be listed on BSE SME. The IPO constitute 27.50% of the post-IPO paid-up capital of the company. From the net proceeds of the equity issue, the company will utilize Rs. 81.50 cr. for working capital, Rs. 61.03 cr. for capex on purchase of plant and machinery, and the rest for general corporate purposes.

The IPO is solely lead managed by GYR Capital Advisors Pvt. Ltd., and Purva Sharegistry (India) Pvt. Ltd. Is the registrar to the issue. Pace Stock Broking Services Pvt. Ltd., is the market maker. Intellect Stock Broking Ltd. is a sub-syndicate member.

After issuing initial equity capital at par value, the company issued/converted further equity shares in the price range of Rs. 470.00 – Rs. 47968.00 per share between October 2024, and January 2026. It has also issued bonus shares in the ratio of 200 for 1 in December 2025. The average cost of acquisition of shares by the promoters is Rs. 0.05 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 12.77 cr. will stand enhanced to Rs. 17.61 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 583.05 cr.

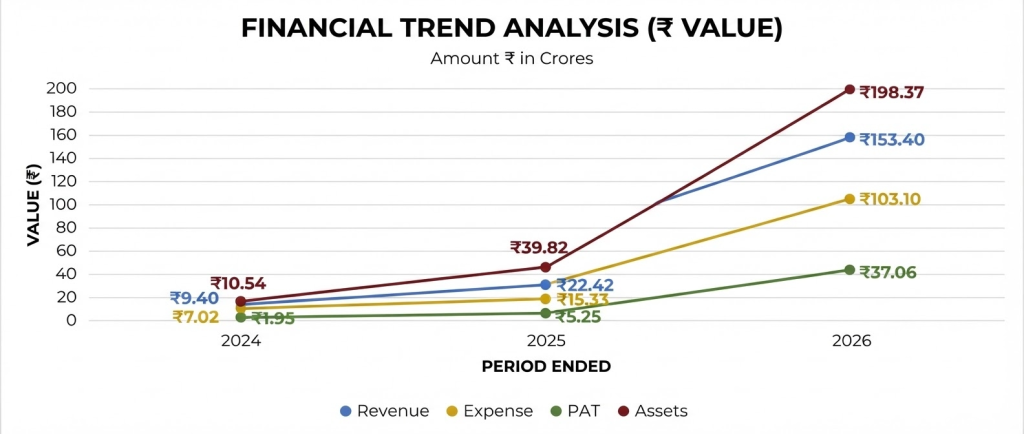

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 9.40 cr. / Rs. 1.95 cr. (FY24), Rs. 22.42 cr. / Rs. 5.25 cr. (FY25), Rs. 153.40 cr. / Rs. 37.06 cr. (FY26). While it posted growth in its top lines for the reported periods, the boosted bottom lines from FY25 onward raises eyebrows and concern over its sustainability going forward. Scaling up of top and bottom line for FY26 is surprising. Its contingent liability of Rs. 23 cr. as of Marach 31, 2026, and rising trade receivables raise alarm.

For the last three fiscals, the company has reported an average EPS of Rs. 17.34 and an average RoNW of 43.90%. The issue is priced at a P/BV of 5.11 based on its NAV of Rs. 64.73 per share as of March 31, 2026, but its post IPO NAV data is missing from its offer documents.

If we attribute FY26 super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 15.73, and based on FY25 earnings, the P/E stands at 111.07. The issue appears aggressively priced based on its recent super earnings.

The company has posted PAT Margins of 20.82% (FY24), 23.75% (FY25), 24.91% (FY26), and ROCE margins of 38.61%, 23.02%, 56.44%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends since incorporation. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has shown Unimech Aerospace and Azad Engg., as its listed peers. They are currently trading at a P/E of 95.2 and 121.0 (as of July 10, 2026). However, they are not truly comparable on an apple to apple basis. This comparison appears to be an eyewash.

This is the 36th mandate from GYR Capital Advisors in the last three fiscals (including ongoing fiscal), and out of the last 11 listings, 2 listed at par, and the rest with premium ranging from 4.92% to 90.0% on the date of listing.

LPIL is one of the leading players in power cables and conductors’ segment in North-East region. It sells its products on PAN India basis. The company improved its margins with backward integration and introduction of new high value/high margin products. The company is repaying around 59% debt, that will bring finance cost savings. Based on its recent financial data, the issue appears fully priced. Well-informed investors can park funds for medium to long term.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.