Aastha Spintex Ltd. (ASL) is engaged in the business of manufacturing and trading of carded, combed and compact combed cotton yarns and cotton bales. In Fiscal 2025, the Company has achieved the highest ROCE and RONW amongst its selected peers. Its cotton bales are utilized both for captive production of cotton yarns and for supply to other spinning units and the cotton yarns produced are used in both knitting and weaving applications, catering to a wide spectrum of end-use segments and products including denim, terry towels, shirting, sheeting, sweaters, socks, bottom wear, home textiles, and industrial fabrics.

It has a semi-automated and integrated spinning and ginning Manufacturing Facility situated at Halvad, Morbi, Gujarat. The company produces 100% cotton yarns in counts ranging from Ne 26 to Ne 40 which includes carded, combed and combed compact varieties ("Ne" refers to the English Cotton Count System, which is a standard way to measure the fineness or thickness of yarn. The higher the Ne, the finer the yarn).

The ginning process converts raw cotton into cotton bales through stages of cleaning and separation, during which cotton seeds and other by-products are generated. While the cleaned lint is pressed into bales for supply to spinning mills, the separated cotton seeds are sold to industries engaged in oil extraction, animal feed, and other applications, thereby providing an additional revenue stream for the Company. A nominal portion of raw cotton is lost as non-recoverable waste during the process.

The spinning of cotton into yarn involves several stages of cleaning, carding and drawing of cotton, during which by-products such as comber, licker-in, and hard waste (collectively, “cotton waste by-products”) are generated. These cotton waste by-products are sold to industries manufacturing non-woven fabrics and open-end yarns, providing an additional revenue stream for the Company. Nominal portion of cotton in the range of 0.1% to 0.3% of the total cotton yarn produced is non-sellable waste.

ASL operates exclusively in the business-to-business (B2B) segment, supplying its products to buyers such as textile manufacturers, yarn exporters, bulk purchasers and fabric processors (collectively “Customers”). Its exclusive B2B focus allows it to streamline production and supply chain processes around the needs of buyers, ensuring consistent quality, delivery, and efficient order fulfilment. It also allows to build long-term client relationships and offer customized yarn solutions tailored to specific technical parameters including count, twist, and strength.

The company primarily sell its products in the domestic market. Its sales within the state of Gujarat are undertaken directly by the Company, whereas the majority of cotton yarn sales to Customers located outside the state of Gujarat are facilitated through a reseller arrangement with 7 Seas Impex. This dual-channel strategy for sale of products, denotes the dual sales framework adopted by the Company which enables it to leverage the operational, regulatory, and logistical capabilities of 7 Seas Impex for markets outside the state of Gujarat (including export markets), thereby allowing the Company to remain focused on its core manufacturing functions, including enhancement of technical capabilities, product quality, and operational efficiency. As of December 31, 2025, it had 205 employees on its payroll.

Accordingly, the reseller structure minimises the requirement for allocation of internal resources toward activities undertaken by 7 Seas Impex and supports timely fulfilment and efficient execution of the Company’s sales operations under the said model.

In line with this strategy, ASL has entered into a Share Purchase Agreement (“SPA”) with Falcon Yarns Private Limited (“Falcon”) and its promoters (collectively, the “Sellers”) for the acquisition of 100% equity shareholding of Falcon. Falcon is engaged in the manufacturing of carded, combed and combed compact cotton yarn and operates a manufacturing facility at Survey No. 177/1, Village Bharudi, NH-27, near Bharudi Toll Plaza, Gondal, Rajkot-360 311, Gujarat, with an annual installed production capacity of 9,757 MT. Post completion of this acquisition, ASL’s total spinning capacity is expected to increase from 7,700 MT per annum to 17,457 MT per annum. Falcon has recorded revenue from operations of Rs. 249.44. cr., Rs. 220.35 cr., and Rs. 228.75 cr., in the last three financial years.

This proposed acquisition is expected to contribute to its inorganic growth objectives, while the increased manufacturing scale, enhanced order-book visibility and broadened customer base are expected to support future organic growth, operational efficiencies and improved market positioning.

The company is coming out with its maiden book building route primary IPO of 12500000 equity shares of Rs. 10 each to mobilize Rs. 170.00 cr. at the upper cap. The company has announced a price band of Rs. 125 – Rs. 136 per equity shares of Rs. 10 each. The issue opens for subscription on June 29, 2026, and will close on July 01, 2026. The minimum application to be made is for 110 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 28.32% of the post-IPO paid-up equity capital. From the net proceeds of the IPO, the company will utilize Rs. 111.51 cr. for part purchase consideration for acquisition of Falcon Yarns Pvt. Ltd., Rs. 10.00 cr. for working capital of Falcon Yarns Pvt. Ltd. as inter-corporate deposits, and the rest for general corporate purposes.

The company has allocated not more than 20% for QIBs, not less than 40% for HNIs and not less than 40% for Retail investors.

The joint Book Running Lead Managers (BRLMs) to this issue are BOI Merchant Bankers Ltd., PNB Investment Services Ltd., and Bigshare Services Pvt. Ltd., is the registrar to the issue. MNM Stock Broking Ltd. is a syndicate member.

The company has issued initial equity shares at par value, and there after issued further equity shares at Rs. 82.50 per share in between August 2024 and September 2025. The average cost of acquisition of shares by the promoters is Rs. 12.14, Rs. 12.48, Rs. 13.12, and Rs. 15.60 per share.

Post-IPO, its current paid-up equity capital of Rs. 31.64 cr. will stand enhanced to Rs. 44.14 cr. Based on the upper cap of the price band, the company is looking for a market cap of Rs. 600.33 cr.

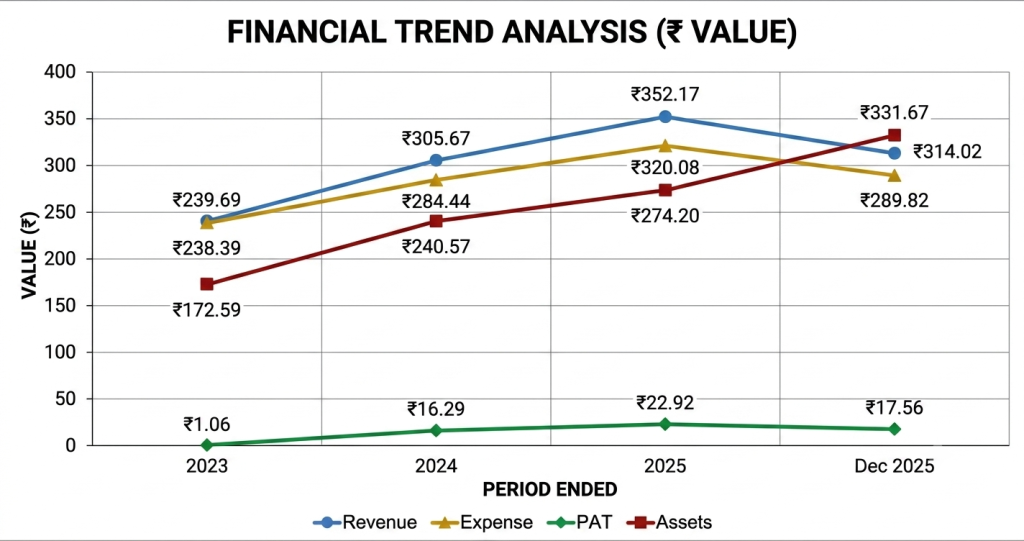

On the financial performance front, for the last three fiscals, the company has posted a total income/net profit, of Rs. 239.69 cr. / Rs. 1.06 cr. (FY23), Rs. 305.67 cr. / Rs. 16.29 cr. (FY24), and Rs. 352.17 cr. / Rs. 22.92 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 17.56 cr. on a total income of Rs. 314.02 cr. The company posted growth in its top and bottom lines for the reported periods. However, the sudden boost in its bottom line from FY24 onwards raise eyebrows and concern over its sustainability going forward, as it is operating in a highly competitive and fragmented segment.

For the last three fiscals, the company has posted an average EPS of Rs. 6.20 and an average RoNW of 17.06 %. The issue is priced at a P/BV of 2.69 based on its NAV of Rs. 50.53 as of December 31, 2025, and at a P/BV of 1.86 based on its post-IPO NAV of Rs. 73.21 per share at the upper cap.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at P/E of 25.66. Based on FY25 earnings, the P/E stands at 26.20. The issue appears aggressively priced despite recent super financial data.

For the reported periods, while the company has posted PAT margins of 0.44% (FY23), 5.34 % (FY24), 6.53% (FY25), 5.60% (9M-FY26), and RoCE margins of 4.58%, 18.95%, 18.89%, 12.13%, respectively for the referred periods. On proforma consolidated basis, it posted PAT Margins of 4.16% (FY25), 4.30% (9M-FY26), and RoCE margins of 19.11%, 13.66% respectively for the said periods.

All amounts in Indian Rupees crores

The company not paid any dividends for the reported periods of the offer document. It has already adopted a dividend policy in August 2025, based on its financial performance and future prospects.

As per the offer document, the company has shown Ambika Cotton Mills, Lagnam Spintex, Pashupati Cotspin, as its listed peers. They are currently trading at a P/E of 13.8, 9.83, and 132 (as of June 25, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

The one BRLM associated with this issue (PNB Investment Services) has handled 2 issues in the last 3 fiscals (including the ongoing one), out of which no issues closed below the offer price on listing date. BOI Merchant Bankers Ltd. has not handled any issues in the said period.

ASL is engaged in the business of manufacturing and trading of various type of cotton yarns and cotton bales. The company is in the process of acquiring 100% equity in Falcon Yarns Pvt. Ltd. The company marked growth in its top and bottom lines for the reported periods. Based on its recent financial data, despite super profits, the issue appears aggressively priced. It is operating in a highly competitive and fragmented segment. . Only well-informed/cash surplus/risk seekers may park moderate funds for long term

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.