Turtlemint Fintech Solutions Ltd. (TFSL) is a tech-enabled insurance distribution platform that connects customers, insurance advisors and insurers. In 2015, Turtlemint became the first to adopt the point-of-sale person (“PoSP”) distribution model and also has the largest certified PoSP network among the Peer Group as of March 31, 2025 as well as December 31, 2025 (Source: Redseer Report).

According to the Redseer Report, it has significantly outpaced the growth of the overall retail insurance market, in terms of gross direct premium income (“GDPI”). While the combined growth rate of retail health, retail life new business, and motor insurance stood at a CAGR of approximately 10.3%

between Fiscals 2020 and 2025, the company achieved a GDPI growth (within the same categories) of approximately 3.00 times higher in the period (Source: Redseer Report). It has demonstrated significant growth in its Platform Premium, growing from Rs. 698.90 cr. in Fiscal 2020 to Rs. 2945.94 cr. in Fiscal 2025, achieving a CAGR of 33.34%, and by 33.63% from Rs. 1969.26 cr. in the nine months period ended December 31, 2024 to Rs. 2631.57 cr. in the nine months period ended December 31, 2025.

The company has facilitated distribution of 21.87 million insurance policies from April 1, 2022 to December 31, 2025 that generated Platform Premium amounting to Rs. 10066.10 cr. across 19,171 pin codes in India, as of December 31, 2025 (representing 97.88% of the total pin codes (i.e., 19,587 pin codes) in India, as of October 2025, according to the Redseer Report). It has onboarded and empowered a large and geographically diversified base of 631,885 Digital Partners, including 507,124 PoSPs, as of December 31, 2025, who have completed the mandatory training, enabling them to obtain the requisite certification to distribute insurance products in accordance with applicable IRDAI regulations, including the Guidelines on Point of Sales Person - Non-Life & Health Insurers (IRDA/ Int/ GDL/ ORD/ 183/ 10/2015) and any subsequent amendments (“PoSP Regulations”). In Fiscal 2025 and the nine months period ended December 31, 2025, TFSL onboarded 99,178 and 87,913 Digital Partners, respectively, further strengthening its distribution presence across India.

According to the Redseer Report, insurance products are inherently complex and hence customers often seek guidance throughout their insurance journey, not just at the time of purchase, but also during post-sale servicing and claims. Recognizing this, the company has focused on building a comprehensive tech-driven, mobile-first platform supported with its physical branch network for its Digital Partners, enabling them to deliver effective advisory services to customers. Its platform equips Digital Partners with tools to manage and grow their business, including product comparison, policy quote generation, training, marketing, lead management, conversion, customer relationship management and post-sales support such as claims management. This integrated approach of its technology platform combined with “on-the-ground” Digital Partners creates a seamless offering to effectively serve customers within their communities. It has made, and intend to continue making, investments in artificial intelligence (“AI”) technologies, including agentic architectures. These investments are intended to enhance Digital Partner productivity, streamline operational processes and expand the scalability of customer support.

Its AI-driven tools are designed to facilitate more personalized advice, accelerate issue resolution and improve service delivery, particularly in underserved markets in India. According to the Redseer Report, the insurance distribution landscape has undergone a fundamental transformation with the rise of digital platforms. Traditionally, insurance was sold primarily through offline channels, individual agents, brokers, and bancassurance (corporate agents – banks and others), often resulting in a fragmented customer experience. However, with the advent of digitization, a new generation of tech-enabled insurance brokers has emerged. These platforms offer a consolidated interface where customers can research, compare and purchase policies across multiple insurers, enhancing accessibility, choice and transparency.

Recognizing that customers still require assistance throughout the insurance journey, especially during product selection and claims, these digital brokers have adopted the POSP model. (Source: Redseer Report). It has established a significant presence in B30+ markets, which refer to the rest of India except Top 30 cities by population (“T30”), according to the Redseer Report. As of March 31, 2025, 82.18% of its Digital Partners are based in B30+ markets and 73.78% of Platform Premium distributed sold in B30+ markets, while as of December 31, 2025, 80.09% of its Digital Partners are based in B30+ markets and 75.13% of Platform Premium distributed sold in B30+ markets. According to the Redseer Report, on the other hand, the industry share of premium from B30+ markets in motor, retail health, and life insurance new business was 50%-60% as of March 31, 2025. Further, B30+ markets are expected to contribute significantly to insurance growth, accounting for 45%–54% of total GDPI from motor insurance with a CAGR of 14%–17%, 37%–43% of health insurance GDPI with a CAGR of 17%–19% and 67%–75% of total life new business GDPI with a CAGR of 10%–11% between Fiscals 2025 and 2030 (Source: Redseer Report). B30+ markets are projected to experience insurance demand growth rates up to 1.6 times higher than T30 between Fiscals 2025 and 2030 for motor, health and life new business insurance (Source: Redseer Report). In addition, TFSL caters to the T30 markets, with 19.91% of its Digital Partners based in these markets, as of December 31, 2025.

By empowering Digital Partners in these markets with its comprehensive suite of digital tools and advisory support, the company is well-positioned to drive insurance adoption and support the Government of India’s broader goal of increasing insurance penetration across India. It has partnered with 45 Insurer Partners, as of December 31, 2025 (representing 75% of all life and general insurers in India, according to the Redseer Report), enabling its Digital Partners to offer customers an unbiased selection of brands and products that address their individual requirements.

Since its inception, it has focused on building an advisory led model to drive insurance penetration in India. While the company has enhanced its capabilities to keep pace with the evolving insurance landscape, its Digital Partners have remained at the core of its product development and platform strategy. This led the company to launching Turtlemint Pro, a mobile and web-based application empowering Digital Partners to sell insurance products in Fiscal 2018. Regulatory developments from the IRDAI enabled broader participation in insurance distribution and facilitated digital onboarding, compliance, and technology adoption, fueling its platform’s growth. As its platform scaled, it identified the need for robust training and lead generation tools for its Digital Partners. This led to the launch of Turtlemint Academy in Fiscal 2018, a comprehensive training tool, and the introduction of Grow in Fiscal 2021, which helps Digital Partners share personalized content, create awareness, and promote insurance literacy.

In Fiscal 2025 and the nine months period ended December 31, 2025, Turtlemint Academy had an average monthly active user (“MAU”) of 52,323 and 56,775 Digital Partners, respectively, and Grow has enabled approximately 2.17 million shares, from April 1, 2024 to December 31, 2025, by Digital Partners to customers. In Fiscal 2021, the company expanded its offerings to include mutual funds, and in Fiscal 2024, expanded to include loans and deposit products. Its advisor-centric approach also attracted additional partnerships with enterprises, leading to the launch of Turtlefin, a digital insurance distribution platform for enterprises, and OneAPI, which allows companies to either embed insurance offerings directly onto their platforms or enables them to digitize their insurance distribution process. Through these initiatives, the company aims to enhance access to insurance and financial products and drive higher insurance penetration across India. As of December 31, 2025, it had 2348 permanent employees on its payroll.

The company is coming out with its maiden book building route combo IPO of 58070398 equity shares of Re. 1 each to mobilize Rs. 882.67 cr. at the upper cap. The IPO consists of fresh equity issue worth Rs. 660.72 cr. (approx. 43468552 equity shares at the upper cap), and Offer for Sale (OFS) of 14601846 equity shares (worth Rs. 221.95 cr. at the upper cap). The company has announced a price band of Rs. 144 – Rs. 152 per equity shares of Re. 1 each. The issue opens for subscription on June 19, 2026, and will close on June 23, 2026. The minimum application to be made is for 98 shares and in multiples thereon, thereafter. Post allotment, shares will be listed on BSE and NSE. The issue constitutes 19.72% of the post-IPO paid-up equity capital. From the net proceeds of the fresh equity issue, the company will utilize Rs. 25.64 cr. for capex on cloud and server related infrastructure, Rs. 193.04 cr. for salary towards technology and product development teams, Rs. 39.07 cr. for marketing initiatives expenditure, Rs. 43.08 cr. for expenditure on lease payment of its properties including its subsidiary TIB, Rs. 128.64 cr. towards investment in it wholly owned subsidiary TIB, and the rest for inorganic growth and general corporate purposes.

The company has allocated not less than 75% for QIBs, not more than 15% for HNIs and not more than 10% for Retail investors.

The four Book Running Lead Managers (BRLMs) to this issue are ICICI Securities Ltd., Jefferies India Pv.t Ltd., JM Financial Ltd., Motilal Oswal Investment Advisors Ltd., and KFin Technologies Ltd., is the registrar to the issue. JM Financial Services Ltd., and Motilal Oswal Financial Services Ltd. are the syndicate members.

After issuing the initial equity shares at par value, the company issued further equity shares in the price range of Rs. 1075 – Rs. 34904 per share (on the basis of Re. 1 FV), between April 2015 and May 2026. It has also issued bonus shares in the ratio of 500 for 1 in July 2025. The average cost of acquisition of shares by the promoters/selling stakeholders is Rs. NA, Rs. 11.64, Rs. 12.00, Rs. 17.30, Rs. 21.12, Rs. 39.88, Rs. 80.95, Rs. 83.47, Rs. 93.54, and Rs. 127.32 per share.

Post-IPO, its current paid-up equity capital of Rs. 25.10 cr. will stand enhanced to Rs. 29.45 cr. Based on the upper cap of the price band, the company is looking for a market cap of Rs. 4476.08 cr.

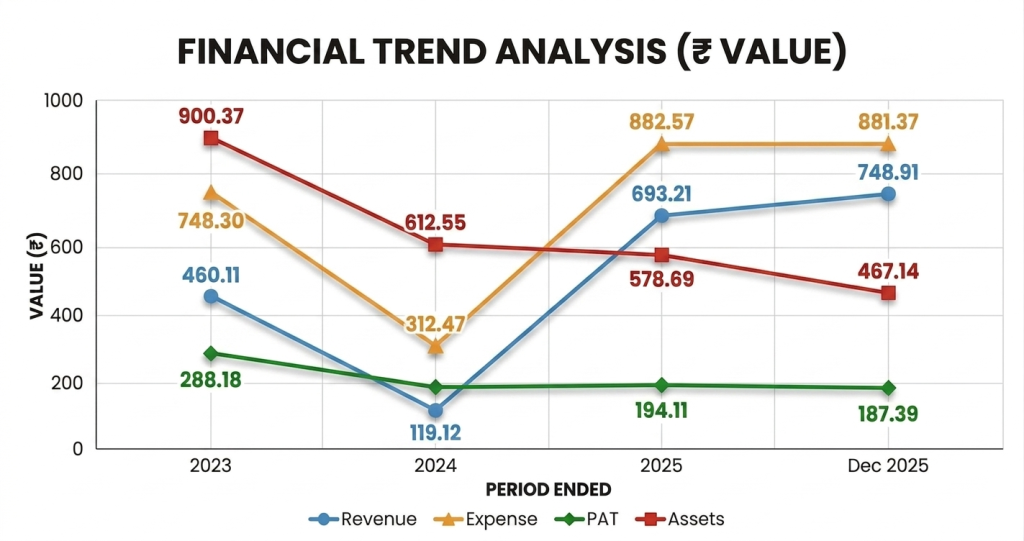

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted a total income/net profit/ - (loss), of Rs. 460.11 cr. / Rs. – (288.18) cr. (FY23), Rs. 119.12 cr. / Rs. – (193.35) cr. (FY24), and Rs. 693.21 cr. / Rs. – (194.11) cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a loss of Rs. – (187.39) cr. on a total income of Rs. 748.91 cr. The fall in its bottom line for 9M-FY26 is including exceptional items worth Rs. 54.93 cr.

According to the management, it is now fully geared with major provisioning and the digital PoSP platform in place and is confident of turning the corner soon and continue to have growing green bottom lines for coming years. It enjoys the most preferred digital partner with most of the insurers and controls major market share with increasing penetrations. The are looking for optimistic performance for coming years with major addition to its bottom lines.

For the last three fiscals, the company has posted an average EPS of Rs. – (7.96 – on restated basis) and an average RoNW of – (41.54) %. The issue is priced at a P/BV of 2.77 based on its NAV of Rs. 54.95 as of December 31, 2025, and at a P/BV of 15.14 on the basis of its post-IPO NAV of Rs. 10.04 per share at the upper cap.

The issue is with a negative NAV since it has posted losses for the reported periods. However, considering their track records and the likely future trends, it is a pure long term bet for well-informed investors.

For the reported periods, PAT Margins and ROCE Margins data is not available as it has been posting losses for the reported periods.

All amounts in Indian Rupees crores

The company not paid any dividends for the reported periods of the offer document. It has already adopted a dividend policy in August 2025, based on its financial performance and future prospects.

As per the offer document, the company has PB Fintech as its listed peer. It is currently trading at a P/E of 111 (as of June 18, 2026). However, they are not truly comparable on an apple-to-apple basis. This comparison appears to be an eyewash.

The four BRLMs associated with this issue have handled 98 issues in the last 3 fiscals (including the ongoing one), out of which 30 issues closed below the offer price on listing date.

TFSL is a tech-enabled insurance distribution platform that enjoys pure leadership in PoSP segment. It enjoys most preferred partner status in digital insurance market amidst entire insurance spectrum. It posted losses for the reported periods and thus the issue is priced at a negative P/E. It has major share in the insurance marketing that spreads in Health, Car and Life insurance business for major clients. With the major expenses in place, its meter is down and the company is placed to enjoy virtual monopoly with rising new as well as renewal business in coming years. TFSL enjoys leadership position in B30+ market place where maximum opportunity prevails. Well-informed investor may park funds for long term, as this is a pure long-term play offer.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.