Diksha Polymers IPO Review (BSE SME)

Diksha Polymers Ltd. (DPL) is engaged in the business of manufacturing PET Bottles/ Containers and PET Preforms. PET Containers are majorly used for storage of beverages, oils, any other ancillary products. PET Preforms is used as a raw material to manufacture PET Containers. The company currently operates through three manufacturing facilities which are located at part of Plot 33, part of 32 (1) and part of 62, Industrial Area, Maharajpura, Gwalior in Madhya Pradesh, India and is spread across 26,879 sq. ft on total basis. As on March 31, 2026, the aggregate installed capacity of its manufacturing plants is 2,163 MTPA for PET bottles and 1,913 MTPA for PET Preforms.

DPL is able to cater to various companies who generally require components of different size and shapes. All the moulding takes place at its facility on machines which has an installed capacity of 2,163 MTPA for PET bottles and 1,913 MTPA for PET Preforms and it mould products ranging from 8gm to 250gms. Its PET Preforms and PET Containers are plastic products manufactured using injection moulding and blow moulding techniques, ensuring precision and durability. PET Containers has application across a wide range of industries, including lubricants, food and beverages, consumer goods, pharmaceuticals, agrochemicals, etc. The company has on-payroll employee strength of 17 persons as on March 31, 2026.

Issue Details / Capital History

The company is coming out with its maiden IPO of 1598400 equity shares of Rs. 10 each at a fixed price of Rs. 112 per share to mobilize Rs. 17.90 cr. The minimum application to be made is for 2400 shares and in multiples of 1200 shares thereon, thereafter. The issue opens for subscription on June 17, 2026 and will close on June 19, 2026. The shares will be listed on BSE SME. The IPO constitute 30.76% of the post-IPO paid-up capital of the company. The company is spending Rs. 1.90 cr. for this IPO process and from the net proceeds of the issue, it will utilize Rs. 13.75 cr. for repayment/prepayment of certain borrowings, Rs. 2.25 cr. for general corporate purposes.

The IPO is solely lead managed by Aryaman Financial Services Ltd., and Cameo Corporate Services Ltd. is the registrar to the issue. Shreni Shares Ltd., is the market maker.

The company has issued entire initial equity capital at par value. It has also issued bonus shares in the ratio of 8 for 1 in June 2025.The average cost of acquisition of shares by the promoters is Rs. NA per share.

Post-IPO, company’s current paid-up equity capital of Rs. 3.60 cr. will stand enhanced to Rs. 5.20 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 58.20 cr.

IPO Lead Managers & Registrar

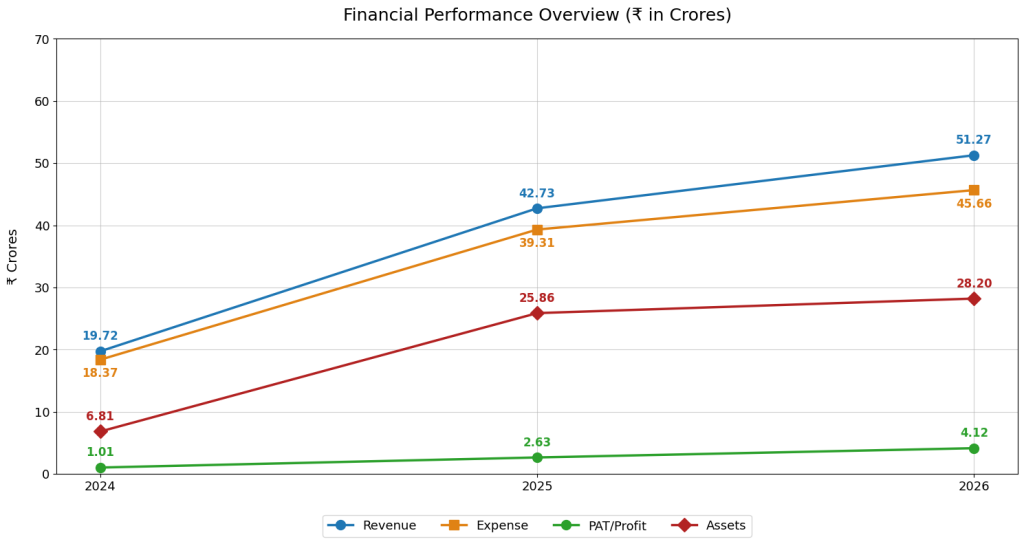

On the financial performance front, for the last three fiscals, the company has posted total income/ net profit, of Rs. 19.72 cr. / Rs. 1.01 cr. (FY24), Rs. 42.73 cr. / Rs. 2.63 cr. (FY25), Rs. 51.27 cr. / Rs. 4.12 cr. (FY26). The company marked growth in its top and bottom lines for the reported periods. Its higher debt-equity ratio raise alarm.

For the last three fiscals, the company has reported an average EPS of Rs. 8.63 and an average RoNW of 53.59%. The issue is priced at a P/BV of 4.73 based on its NAV of Rs. 23.68 per share as of March 31, 2026, and at a P/BV of 2.20 based on its post IPO NAV of Rs. 50.85 per share.

If we attribute FY26 super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 14.14, and based on FY25 earnings, the P/E stands at 22.13. The issue appears aggressively priced based on its recent earnings. The trade receivable has increased on year-on-year basis.

The company has posted PAT Margins of 5.13% (FY24), 6.16% (FY25), 8.03% (FY26), and ROCE margins of 26.54%, 23.52%, 28.09%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends since its incorporation. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

Comparison with Listed Peers

As per the offer document, the company has shown TPL Plastech, Mitsu Chem Plast, as its listed peers. They are trading at a P/E of 18.0 and 12.6 (as pf June 12, 2026). However, they are not truly comparable on an apple-to-apple basis. This compare appears as an eyewash.

Merchant Banker's Track Record

This is the 17th mandate from Aryaman Financial in the last four fiscals (including the ongoing one). Out of the last 10 listings, 1 listed at discount, and the rest with premium ranging from 0.83% to 20.19% on the listing date.

Conclusion

DPL is engaged in the business of manufacturing PET Bottles/Containers and PET Performs. The product is widely used by many industry segments for storage of beverages, oils, etc. The company marked growth in its top and bottom lines for the reported periods. Based on its recent financial data, the issue appears aggressively priced. Tiny paid-up equity capital post-IPO indicates longer gestation period for migration. There is no harm in skipping this pricey and dicey offer.

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.