Autofurnish Ltd. (AL) is engaged in the manufacturing and trading of automotive accessories, the company is operating primarily in the B2B segment and the entire revenue has been derived solely from the B2B segment, engaged in the design, manufacturing, marketing and sale of automobile accessories, with a core product line that includes body covers and foot mats for both cars and two-wheelers.

The Company’s revenue from manufacturing activities, as disclosed above, is inclusive of revenue generated from its design segment. Mainly its products are marketed under the brand name “Autofurnish, and “Mototrance” catering to a wide range of industries. AL’s team works closely with clients to develop customized products that meet specific design requirements. Its manufacturing facilities are certified under ISO 9001:2015, ISO 14001:2015, ISO 50001:2018, ISO 45001:2018, ISO 26262-1:2011, IATF 16949:2016 and Good Manufacturing Practices (GMP), reflecting its commitment to quality, safety, and sustainability.

Over the years, it has not only maintained strong relationships with existing customers but also expanded its customer base, increasing from approximately 53 customers in Fiscal 2024 to approximately 106 customers in Fiscal 2025. Over time, AL has evolved into a one-stop solution for automotive accessories, offering a diverse product portfolio that combines both manufacturing and trading. Its wholly owned subsidiary, Golden Mace Private Limited is engaged in trading of automotive accessories and focuses on the B2C segment through online platforms such as Flipkart, Amazon, Zepto and its website. As of March 31, 2026, it had 40 employees on its payroll.

The company is coming out with its maiden IPO of 3561000 equity shares of Rs. 10 each at a fixed price of Rs. 41 per share to mobilize Rs. 14.60 cr. The minimum application to be made is for 6000 shares and in multiples of 3000 shares thereon, thereafter. The issue opens for subscription on May 21, 2026 and will close on May 25, 2026. The shares will be listed on BSE SME. The IPO constitute 26.34% of the post-IPO paid-up capital of the company. The company is spending Rs. 1.45 cr. for this IPO process. From the net proceeds of the equity issue, it will utilize Rs. 1.89 cr. for capex on new machineries, Rs. 9.30 cr. for working capital, and Rs. 1.96 cr. for general corporate purposes.

The IPO is solely lead managed by Novus Capital Advisors Pvt. Ltd., and Skyline Financial Services Pvt. Ltd. is the registrar to the issue. NDA Securities Ltd. is the market maker.

After issuing initial equity capital at par value, it issued further equity shares at a fixed price in the price range of Rs. 29 – Rs. 41 per share between August 2024 – March 2025. It has also issued bonus shares in the ratio of 16 for 1 in June 2024. The average cost of acquisition of shares by the promoters is Rs. 45.49 per share.

Post-IPO, company’s current paid-up equity capital of Rs. 9.95 cr. will stand enhanced to Rs. 13.52 cr. Based on the upper band of the IPO pricing, the company is looking for a market cap of Rs. 55.41 cr.

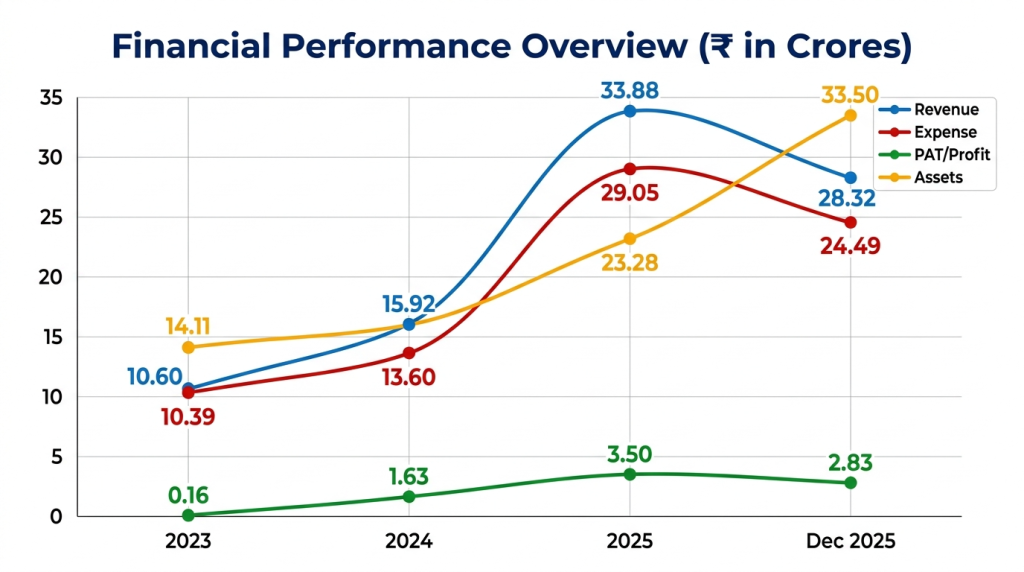

On the financial performance front, for the last three fiscals, the company has (on a consolidated basis) posted total income/ net profit, of Rs. 10.60 cr. / Rs. 0.16 cr. (FY23), Rs. 15.92 cr. / Rs. 1.63 cr. (FY24), Rs. 33.88 cr. / Rs. 3.50 cr. (FY25). For 9M of FY26 ended on December 31, 2025, it earned a net profit of Rs. 2.83 cr. on a total income of Rs. 28.32 cr. The company marked quantum jump in its bottom lines from FY24 onward. Sustainability of such margins going forward remains concern, as it is operating in a highly competitive and fragmented segment.

For the last three fiscals, the company has reported an average EPS of Rs. 2.56 and an average RoNW of 18.00%. The issue is priced at a P/BV of 2.32 based on its NAV of Rs. 17.65 per share as of December 31, 2025, and at a P/BV of 1.72 based on its post-IPO NAV of Rs. 23.81 per share.

If we attribute FY26 annualized super earnings to its post-IPO fully diluted paid-up equity capital, then the asking price is at a P/E of 14.70, and based on FY25 earnings, the P/E stands at 15.83. The issue appears fully priced based on its recent earnings.

The company has posted ROCE Margins of 6.84% (FY23), 28.10% (FY24), 33.74% (FY25), 21.34% (9M-FY26), and PAT margins of 1.49%, 10.24%, 10.51%, 9.99%, respectively for referred periods.

All amounts in Indian Rupees crores

The company has not paid any dividends for the reported periods of the offer document. It will adopt a prudent dividend policy, based on its financial performance and future prospects.

As per the offer document, the company has no listed peers to compare with.

This is the 13th mandate from Novus Capital in the last four fiscals (including the ongoing one). Out of the last 10 listings, 4 opened at discount, 1 at par, and the rest with premium ranging from 2.09% to 31.25% on the date of listing. Thus, the lead manager has an average record.

AL is engaged in the manufacturing and marketing of automotive accessories. It operates in B2B and B2C segments. It posted growth in its top and bottom lines for the reported periods. Based on its recent financial data, the issue appears fully priced. It is operating in a highly competitive and fragmented segment. Only well-informed/cash surplus/risk seekers may park moderate funds for medium term.

Review By on May 17, 2026

Dilip Davda is a veteran financial journalist associated with the Indian stock market since 1978. He has been contributing to print and electronic media on capital markets, insurance, and finance since 1985.

He is widely recognized for reviewing public issues and non-convertible debentures (NCDs) in the primary market. Drawing on over three decades of market experience and close interaction with merchant bankers, his reviews focus on detailed fundamental and financial analysis of companies, with a special emphasis on SME public issues.

Disclaimer: The information provided herein is solely for educational and informational purposes and does not constitute an offer, solicitation, or recommendation to buy or sell any securities. Readers are advised to consult a qualified financial advisor before making any investment decisions. Investments in the securities market are subject to market risks. The author does not intend to invest in the securities discussed.